UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of The Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant ☐

Filed by a Party other than the Registrant ☒

Check the appropriate box:

| ☐ | Preliminary Proxy Statement |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ☐ | Definitive Proxy Statement |

| ☒ | Definitive Additional Materials |

| ☐ | Soliciting Material Under Rule 14a-12 |

| HUNTSMAN CORPORATION |

(Name of Registrant as Specified in Its Charter) |

STARBOARD VALUE LP STARBOARD VALUE AND OPPORTUNITY MASTER FUND LTD STARBOARD VALUE AND OPPORTUNITY S LLC STARBOARD VALUE AND OPPORTUNITY C LP STARBOARD P FUND LP STARBOARD VALUE P GP LLC STARBOARD VALUE R LP STARBOARD VALUE AND OPPORTUNITY MASTER FUND L LP STARBOARD VALUE L LP STARBOARD VALUE R GP LLC STARBOARD LEADERS ECHO II LLC STARBOARD LEADERS FUND LP STARBOARD VALUE A LP STARBOARD VALUE A GP LLC STARBOARD X MASTER FUND LTD STARBOARD G FUND, L.P. STARBOARD VALUE GP LLC STARBOARD PRINCIPAL CO LP STARBOARD PRINCIPAL CO GP LLC JEFFREY C. SMITH PETER A. FELD JAMES L. GALLOGLY SANDRA BEACH LIN SUSAN C. SCHNABEL |

(Name of Persons(s) Filing Proxy Statement, if Other Than the Registrant) |

Payment of Filing Fee (Check the appropriate box):

| ☒ | No fee required. |

| ☐ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: |

| (2) | Aggregate number of securities to which transaction applies: |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) | Proposed maximum aggregate value of transaction: |

| (5) | Total fee paid: |

| ☐ | Fee paid previously with preliminary materials: |

☐ Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing.

| (1) | Amount previously paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing Party: |

| (4) | Date Filed: |

Starboard Value LP, together with the other participants named herein (collectively, “Starboard”), has filed a definitive proxy statement and accompanying BLUE proxy card with the Securities and Exchange Commission to be used to solicit votes for the election of its slate of highly-qualified director nominees at the 2022 annual meeting of stockholders of Huntsman Corporation, a Delaware corporation.

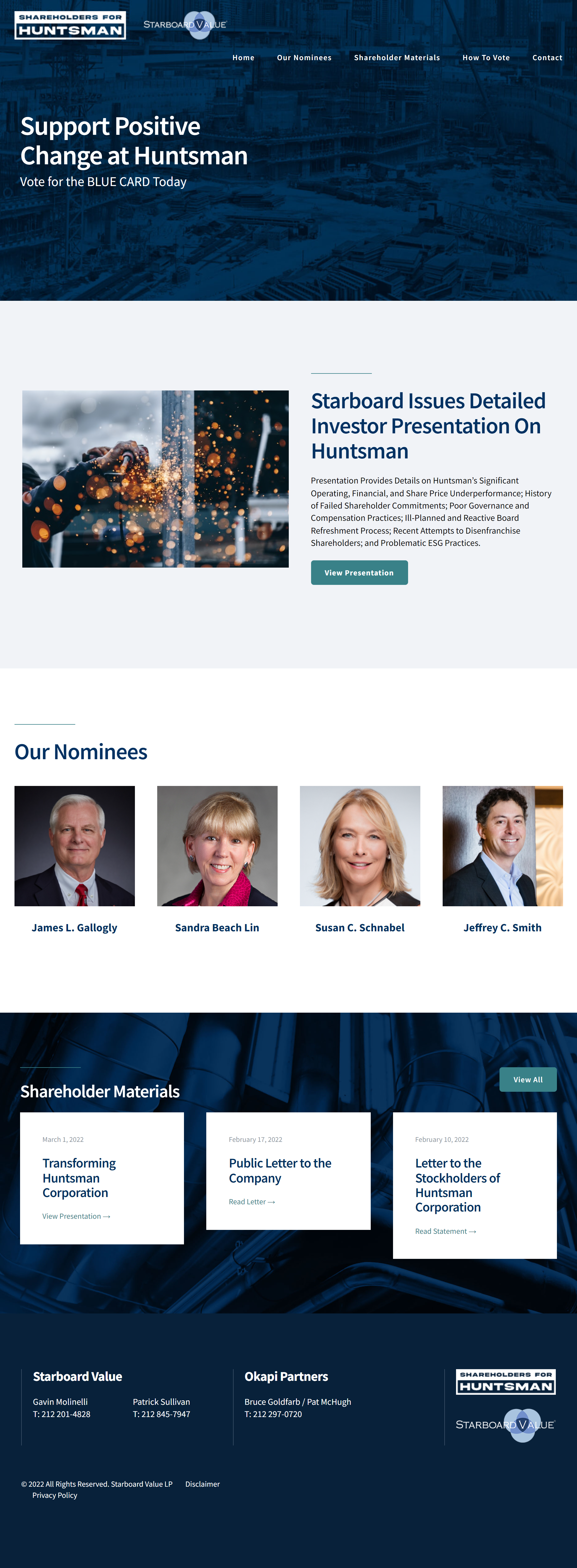

Item 1: On March 1, 2022, Starboard issued the following press release:

Starboard ISSUES DETAILED investor PRESENTATION ON HUNTSMAN

Presentation Provides Details on Huntsman’s Significant Operating, Financial, and Share Price Underperformance;

History of Failed Shareholder Commitments;

Poor Governance and Compensation Practices;

Ill-Planned and Reactive Board Refreshment Process;

Recent Attempts to Disenfranchise Shareholders; and

Problematic ESG Practices

Outlines Operational Improvement Opportunities to Help Drive Improved Performance

Urges Shareholders to Vote FOR Starboard’s Slate of Highly-Qualified and Experienced Nominees on Starboard’s BLUE Proxy Card TODAY

NEW YORK, NY March 1, 2022 /PRNewswire/ -- Starboard Value LP (together with its affiliates, “Starboard” or “we”), one of the largest shareholders of Huntsman Corporation (NYSE: HUN) (“Huntsman” or the “Company”), with an ownership interest of approximately 8.8% of the Company’s outstanding shares, today announced that it has issued a detailed presentation titled “Transforming Huntsman Corporation,” outlining Starboard’s views on Huntsman, the challenges that plagued the Company historically and continue to exist today, opportunities to drive improved performance, and details surrounding Starboard’s slate of highly-qualified and experienced director nominees for election to the Huntsman Board of Directors (the “Board”) at the Company’s upcoming 2022 Annual Meeting of Shareholders (the “Annual Meeting”).

The full presentation, Transforming Huntsman Corporation, can be found at https://www.starboardvalue.com/wp-content/uploads/Starboard_Value_LP_HUN_Shareholder_Presentation_03.01.2022.pdf

Below are some highlights from Starboard’s detailed presentation.1

| · | From February 2005, when CEO Peter Huntsman took the Company public, through Starboard’s Schedule 13D filing in September 2021, the Company has significantly underperformed its peers, and both the chemicals and broader market indices, including a shocking ~562% deficit to the Company’s Performance Peers during this time. |

| · | Since January 2018 when Peter Huntsman assumed the role of Chairman through Starboard’s Schedule 13D filing in September 2021, the Company’s share price has not only continued to underperform its Performance Peers and other relevant indices, including a ~26% deficit to its Performance Peers, but has generated negative shareholder returns during this time. |

1Please refer to the full presentation available at www.shareholdersforhuntsman.com for additional details, disclosures, supporting data, identity of peers, defined terms, underlying assumptions and other relevant information.

| · | With few exceptions, since 2018, Huntsman has been valued at a ~2.0x discount to its peers, with the gap widening significantly post-pandemic in 2021. |

| · | Long-term organic revenue growth in each of the Company’s reporting segments has failed to reach the Company’s target of 2.0x GDP. |

| · | The Company’s profitability has not meaningfully improved since its IPO, and continues to trail both its Performance and Primary Peers. The Adjusted EBITDA margin gap between Huntsman and its peers has continued to widen over time. |

| · | The Company describes 2021 financial results as being the best in the Company’s history, yet Adjusted EBITDA margins and Adjusted EBITDA to free cash flow conversion remain one of the worst among peers. In addition, each of the Company’s three Primary Peers also had record results in 2021, which leads us to believe that the Company’s performance has been driven more by macro conditions rather than skillful execution. |

| · | Prior to hosting its 2021 Investor Day, the Company had made financial commitments to shareholders at three consecutive investor days (2014, 2016, and 2018), and failed to deliver on all three targets. |

| · | 2014 Investor Day |

| û | Failed to achieve $2.0 billion of Adjusted EBITDA over 2- 3 years. |

| û | Adjusted EBITDA actually declined by more than $350 million between 2014 and 2016, ending with only $1.1 billion, which was approximately 44% below the $2.0 billion target that had previously been presented to shareholders. |

| · | 2016 Investor Day |

| û | Failed to achieve $1.3 billion of Adjusted EBITDA in its core non-TiO2 businesses by 2017. |

| · | 2018 Investor Day |

| û | Failed to improve share price performance to ~$60 per share by 20202 (and share price actually declined by 21% between the 2018 Investor Day and December 31, 2020). |

| û | Sold its stake in Venator Materials PLC (“Venator”) for only $140 million, which was $860 million less than what had been promised to shareholders. |

| û | Failed to achieve its $1.7 billion cumulative free cash flow target between 2018 and 2022. |

| · | The Board has consistently set Adjusted EBITDA compensation targets, management’s primary annual cash bonus metric, well below targets that the Company had communicated to shareholders at its various Investor Days. |

| · | We believe the Company’s track record of missed promises has caused the Company’s stock price underperformance and underscores the Board’s repeated failure to hold management accountable. |

| · | The Company hosted yet another Investor Day in 2021 and is making even more promises to shareholders. We question why shareholders should believe the Company’s promises will finally be fulfilled. Without change and significantly greater oversight, we believe shareholders will be incredibly disappointed yet again. |

2 The Company’s closing share price on the day prior to the 2018 Investor Day was $32.02. The Company committed to improving share price by at least $27 per share by 2020, which implied a 2020 target share price of approximately $60 per share by December 31, 2020.

| · | Prior to Starboard’s engagement with the Company, Huntsman had an incredibly entrenched Board with numerous professional, financial, and personal interconnects between both its members and/or the Huntsman family, which we believe created an insular boardroom environment lacking true independence. A few of the numerous conflicts include: |

| û | Dr. Mary Beckerle, who is the CEO of the Huntsman Cancer Institute (“HCI”), which was founded by the Huntsman family and continues to receive substantial funding from the Huntsman Cancer Foundation, of which Peter Huntsman is Chairman and CEO. The Huntsman family has donated almost $750 million to HCI which employs and pays Dr. Beckerle approximately $1 million per year. In addition, Dr. Beckerle was actually terminated from her position as CEO of HCI several years ago and the Huntsman family interceded to have her reinstated by threatening to withhold over $250 million in donations. |

| û | Daniele Ferrari, who was a former executive of Huntsman for fourteen years, then became a board member of both Huntsman and Venator (as a Venator board member, he oversaw a stock price decline of 90%), joined SK Capital as a Senior Director right after the private equity fund accumulated greater than $100 million in unrealized gains from purchasing Huntsman’s stake in Venator for significantly less than what Huntsman had promised its shareholders the stake would be worth. For context, Huntsman promised shareholders its Venator stake would be worth at least $1 billion, and ultimately only received $140 million after conducting a fire sale in late-2020 to SK. |

| · | This interconnected Board repeatedly classified Dr. Beckerle as independent despite these glaring conflicts and repeatedly waived the mandatory retirement policy for other interconnected and long-tenured directors, among other governance failures. |

| · | After avoiding any real refreshment for years, and only after facing pressure from Starboard, the Board rushed through an abrupt and ill-planned refreshment process of some long-tenured directors, replacing them with three new directors, two of whom have had no prior public company board experience. |

| û | In particular, we are highly concerned by the appointment of José Muñoz who not only has never had prior public company board experience, but also has highly questionable circumstances surrounding his departure from Nissan, his former employer. |

| û | Mr. Muñoz worked at Nissan from 2004 to 2019. His time at Nissan coincided with Carlos Ghosn’s tenure, who was CEO from 2001 to 2018. Mr. Muñoz reported directly to Mr. Ghosn as Chief Performance Officer (2016 – 2019). In November 2018, Mr. Ghosn was arrested and fired from Nissan after alleged financial misconduct. Following Mr. Ghosn’s arrest, Mr. Muñoz resigned from Nissan in January 2019. Mr. Muñoz was offered $12.8 million to cooperate with prosecutors to hold Mr. Ghosn accountable, but declined. |

| û | We are highly concerned that Mr. Muñoz apparently refused to participate in efforts to help his former employer hold a member of management accountable for alleged misconduct. |

| · | The Board’s reactive and ill-planned refreshment process also failed to address two of its most conflicted directors - Dr. Beckerle and Mr. Ferrari – both of whom the Board shockingly continues to classify as independent. |

| · | Even with the new directors appointed in January 2022, we believe the Board has already actively disenfranchised shareholders and opted into poor governance practices, including by: |

| û | Shortening the nomination window for shareholders from ~30 days to 10 days; |

| û | Refusing repeated requests to use a universal proxy card despite it being widely considered governance best practice; and |

| û | Badgering Starboard and its nominees with repeated legal letters. |

| · | These aggressive and shareholder unfriendly actions have been taken under the leadership of Cynthia Egan, the Company’s new Lead Independent Director, and we believe perpetuate a highly concerning pattern of poor governance that has occurred under Ms. Egan’s tenure on other Boards. |

| û | As a member of the Governance Committee at BTZ, a taxable fixed income closed-end fund, Ms. Egan allowed BTZ to: 1) unilaterally amend BTZ’s bylaws without a shareholder vote; 2) implement a staggered board despite BTZ having previously had an annually elected board; and 3) alter the voting standard for elections from a plurality standard to a dual voting standard (plurality in uncontested elections and majority of shares outstanding in a contested election). |

| û | In addition, when Saba Capital (“Saba”) attempted to nominate new individuals to BTZ’s board, Ms. Egan along with the rest of BTZ’s board sent Saba additional information requests and ultimately disqualified Saba’s nominees from election, thereby eliminating shareholders’ ability to select the Board that they believe would best represent their interests. We believe Ms. Egan has attempted the same tactics at Huntsman in an attempt to disenfranchise shareholders. |

| · | Leading proxy advisory firms, Institutional Shareholder Services Inc. and Glass, Lewis & Co., LLC, have previously highlighted that the Board has granted the CEO top quartile pay despite bottom quartile performance relative to Proxy Peers. |

| · | Other aspects of the Board and the Compensation Committee’s troubling compensation practices, include: |

| û | Setting compensation targets below investor day promises; |

| û | Revising management’s Adjusted EBITDA target by 40% in the middle of 2020, the only company among Proxy Peers to make such a reduction; |

| û | Selecting an inappropriate peer set to benchmark executive compensation; |

| û | Skewing payout structure favoring higher bonuses; |

| û | Engaging in questionable performance peer selection practices; and |

| û | Approving concerning corporate perquisites. |

| · | Huntsman not only has the worst ESG rating among Primary Peers, but is also unique in being the only company among its Primary Peers to have a recent ratings downgrade. |

| · | We are concerned that the Company’s environmental goals lack rigor and vision, leaving it underprepared for future regulatory and competitive pressure. |

| · | Under the failed oversight of the Board’s ESG Committee, Huntsman has reactively made a carbon neutral pledge and an unfulfilled promise of TCFD reporting in order to, in our view, appease institutional investors. |

| · | Many of Huntsman’s largest shareholders have, for years, publicly called for TCFD-aligned disclosures, yet under the Board’s failed oversight, such information has yet to be disclosed. |

| · | Huntsman, in contrast to its Primary Peers, does not provide investors or employees a fulsome view into the Company’s current workforce composition or practices. |

| · | We believe there are attractive opportunities to improve commercial execution, reallocate corporate resources, and streamline both manufacturing, supply chain, and other operating expenses. |

| · | We believe that Huntsman can improve its Adjusted EBITDA margin by ~600bps on a run rate basis. |

| · | Collectively, our nominees are industry-leading experts with extensive experience in chemical operations, corporate governance, mergers and acquisitions, and capital markets. |

| · | James L. Gallogly |

| ü | Mr. Gallogly is widely considered to be one of the most successful chemical industry operating executives. He has significant operating, financial, and environmental management experience as a senior executive within the chemicals industry, as well as his significant public company board experience would make him a valuable addition to the Board. |

| ü | Mr. Gallogly previously served as Chief Executive Officer and Chairman of the Management Board at LyondellBasell Industries N.V. (“LYB”), a global plastics, chemical, and refining company from 2009 to 2015. During his tenure at Lyondell, the company’s stock price outperformed the S&P Chemicals and S&P 500 indices by 360% and 381%, respectively. |

| ü | Prior to LYB, Mr. Gallogly served as Executive Vice President of each major business unit at ConocoPhillips. Prior to ConocoPhillips, Mr. Gallogly served as Chief Executive Officer Chevron Phillips Chemical Company, a global plastics and chemical company. |

| ü | Mr. Gallogly currently serves as Vice Chairman of the University Cancer Foundation Board of Visitors at the University of Texas M.D. Anderson Cancer Center. |

| ü | Mr. Gallogly previously served as a director of Continental Resources, Inc. and E.I. du Pont de Nemours and Company. |

| · | Sandra Beach Lin |

| ü | Ms. Lin’s significant leadership experience as a senior executive in both the hybrid chemicals and broader industrials industries, coupled with her considerable experience serving on public company boards, would make her a valuable addition to the Board. |

| ü | Ms. Lin is the former President and Chief Executive Officer of Calisolar, a global leader in the production of solar silicon. |

| ü | Previously, Ms. Lin was Executive Vice President of Celanese, a global hybrid chemical company. Celanese is one of Huntsman’s Primary Peers, and a company whose Adjusted EBITDA margins in 2021 were double those of Huntsman. |

| ü | Prior to Celanese, Ms. Lin held various senior executive positions at Avery Dennison, Alcoa, and Honeywell International. |

| ü | Ms. Lin currently serves as a director at Avient Corporation, American Electric Power Company, Trinseo S.A., Ripple Therapeutics, and Interface Biologics. At Trinseo S.A., Ms. Lin serves as Chair of the Environmental, Health, Safety, Sustainability and Public Policy Committee, and at American Electric Power Company, Ms. Lin serves as Chair of the Corporate Governance Committee. |

| ü | We believe Ms. Lin’s impressive accomplishments and relevance to the Company have already been acknowledged by the Board given their openness to having her join as a director during Starboard’s attempts to reach a settlement with the Company earlier this year. |

| · | Susan C. Schnabel |

| ü | Ms. Schnabel’s substantial business experience and financial background, coupled with her extensive experience serving as a director of public and private companies, would make her a valuable addition to the Board. |

| ü | Ms. Schnabel is the Co-Founder and Co-Managing Partner of aPriori Capital Partners. Previously, Ms. Schnabel served as Managing Director of Credit Suisse Asset Management and Co-Head of DLJ Merchant Banking. Prior to that, Ms. Schnabel served as Chief Financial Officer of PetSmart. |

| ü | Ms. Schnabel currently serves as a director of Altice USA, Chair of the Audit Committee of Kayne Anderson BDC, a Trustee of Cornell University, and a director of various other university and non-profit Boards of Directors. |

| ü | Ms. Schnabel previously served as a director of Versum Materials, STR Holdings, Neiman Marcus, Pinnacle Gas Resources, Rockwood Holdings, Shoppers Drug Mart Corporation (TSX), and other private company Boards of Directors. |

| ü | Ms. Schnabel has extensive chemicals industry experience both as an investor and as a board member. She was a key investor and board member during the transformative stages of Rockwood Holdings, a specialty chemicals company whose stock price between IPO and its eventual sale to Albemarle Corporation outperformed the S&P Chemicals and S&P 500 indices by 143% and 223%, respectively.3 |

| · | Jeffrey C. Smith |

| ü | Mr. Smith’s extensive knowledge of the capital markets, corporate finance, and public company governance practices, together with his significant public company board experience, would make him a valuable addition to the Board. |

| ü | Mr. Smith is a Managing Member, Chief Executive Officer, and Chief Investment Officer of Starboard Value LP. Prior to founding Starboard, he was a Partner Managing Director of Ramius LLC, and the Chief Investment Officer of Ramius Value and Opportunity Master Fund Ltd. |

| ü | Mr. Smith currently serves as Chair of the Board of Directors of Papa John’s International, and as a director of Cyxtera Technologies. |

| ü | Mr. Smith previously served as Chair of the Board of Directors of Advance Auto Parts, Darden Restaurants, and Phoenix Technologies. In addition, Mr. Smith has also served as a director of many other public companies. |

HUNTSMAN NEEDS STRONG INDEPENDENT BOARD MEMBERS WHO WILL DEMAND IMPROVED PERFORMANCE AND HELP MAXIMIZE SHAREHOLDER VALUE

We believe you will find our comprehensive presentation to be helpful in understanding the severity of the issues currently plaguing the Company and, importantly, why we believe the election of our superior slate of nominees is required to help drive improved performance and a culture of accountability at Huntsman.

VOTE THE BLUE PROXY CARD TODAY

Please support our efforts to revitalize Huntsman by voting on the BLUE proxy card to elect our slate of highly qualified nominees at the upcoming Annual Meeting.

3 Returns are adjusted for dividends and measured from August 16, 2005, the date of Rockwood’s IPO, through January 12, 2015, the date that Rockwood’s sale to Albemarle was completed.

Our detailed presentation and other important information and materials regarding the Annual Meeting can be viewed at www.shareholdersforhuntsman.com.

If you have any questions or need further assistance with voting your Huntsman shares, please contact Okapi Partners LLC at the phone numbers or email listed below.

Shareholders may call toll-free: (877) 629-6356

Banks and brokers call: (212) 297-0720

E-mail: info@okapipartners.com

About Starboard Value LP

Starboard Value LP is a New York-based investment adviser with a focused and differentiated fundamental approach to investing primarily in publicly traded U.S. companies. Starboard seeks to invest in deeply undervalued companies and actively engage with management teams and boards of directors to identify and execute on opportunities to unlock value for the benefit of all shareholders.

Investor contacts:

Gavin Molinelli, (212) 201-4828

Patrick Sullivan, (212) 845-7947

www.starboardvalue.com

Okapi Partners

Bruce H. Goldfarb/Patrick McHugh

(212) 297-0720

Item 2: On March 1, 2022, Starboard uploaded the following materials to www.shareholdersforhuntsman.com: