UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of The Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant ☐

Filed by a Party other than the Registrant ☒

Check the appropriate box:

| ☐ | Preliminary Proxy Statement |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ☐ | Definitive Proxy Statement |

| ☒ | Definitive Additional Materials |

| ☐ | Soliciting Material Under Rule 14a-12 |

| HUNTSMAN CORPORATION |

(Name of Registrant as Specified in Its Charter) |

STARBOARD VALUE LP STARBOARD VALUE AND OPPORTUNITY MASTER FUND LTD STARBOARD VALUE AND OPPORTUNITY S LLC STARBOARD VALUE AND OPPORTUNITY C LP STARBOARD P FUND LP STARBOARD VALUE P GP LLC STARBOARD VALUE R LP STARBOARD VALUE AND OPPORTUNITY MASTER FUND L LP STARBOARD VALUE L LP STARBOARD VALUE R GP LLC STARBOARD LEADERS ECHO II LLC STARBOARD LEADERS FUND LP STARBOARD VALUE A LP STARBOARD VALUE A GP LLC STARBOARD X MASTER FUND LTD STARBOARD G FUND, L.P. STARBOARD VALUE GP LLC STARBOARD PRINCIPAL CO LP STARBOARD PRINCIPAL CO GP LLC JEFFREY C. SMITH PETER A. FELD JAMES L. GALLOGLY SANDRA BEACH LIN SUSAN C. SCHNABEL |

(Name of Persons(s) Filing Proxy Statement, if Other Than the Registrant) |

Payment of Filing Fee (Check the appropriate box):

| ☒ | No fee required. |

| ☐ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: |

| (2) | Aggregate number of securities to which transaction applies: |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) | Proposed maximum aggregate value of transaction: |

| (5) | Total fee paid: |

| ☐ | Fee paid previously with preliminary materials: |

☐ Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing.

| (1) | Amount previously paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing Party: |

| (4) | Date Filed: |

Starboard Value LP, together with the other participants named herein (collectively, “Starboard”), has filed a definitive proxy statement and accompanying BLUE proxy card with the Securities and Exchange Commission to be used to solicit votes for the election of its slate of highly-qualified director nominees at the 2022 annual meeting of stockholders of Huntsman Corporation, a Delaware corporation (the “Company”).

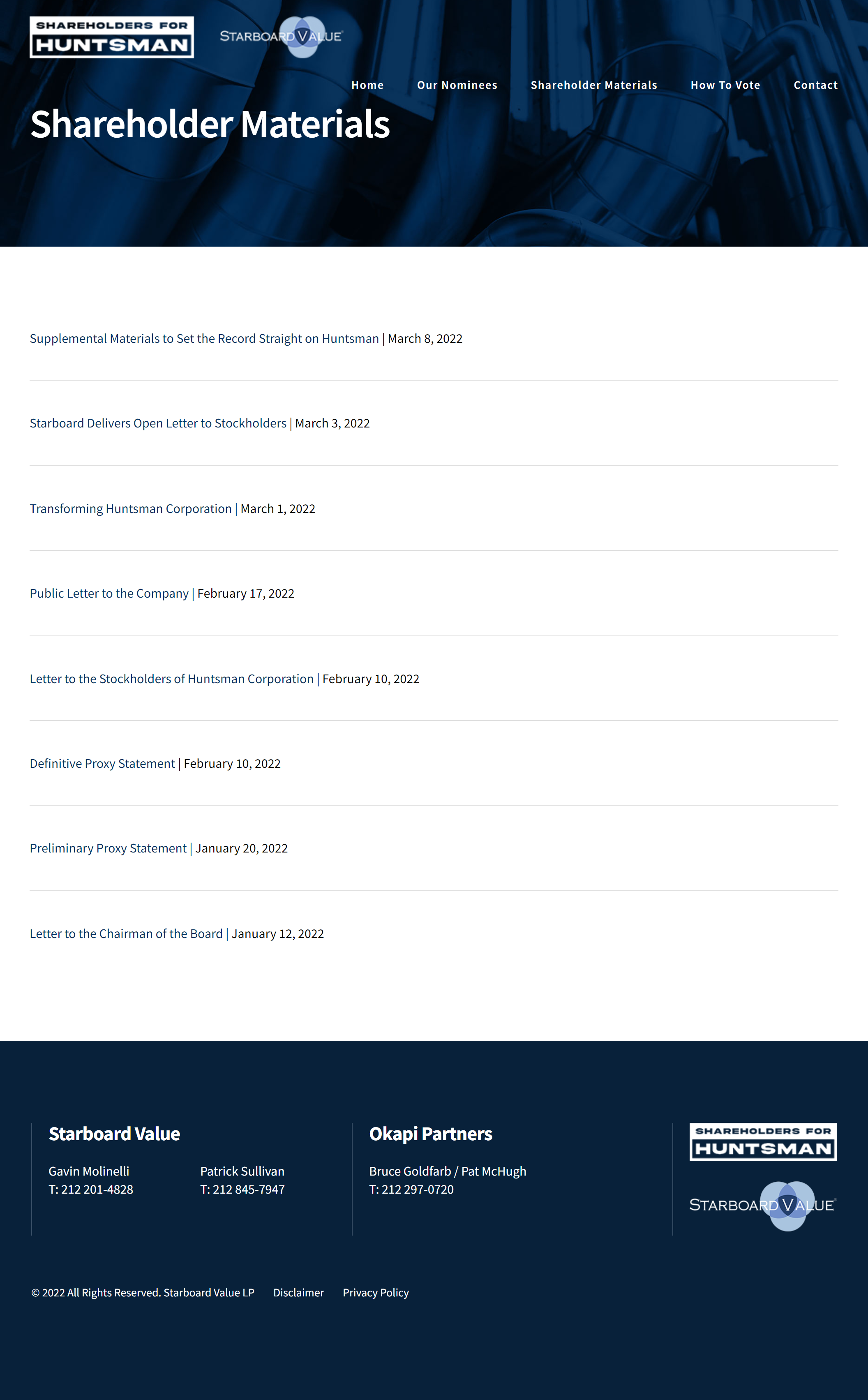

Item 1: On March 8, 2022, Starboard issued a supplemental presentation, a copy of which is attached hereto as Exhibit 1 and is incorporated by reference.

Item 2: On March 8, 2022, Starboard issued the following press release, announcing that Starboard issued a supplemental presentation responding to various false and misleading statements and mischaracterizations made by the Company in its recent investor presentation:

STARBOARD ISSUES SUPPLEMENTAL MATERIALS TO ADDRESS CERTAIN FALSE AND MISLEADING STATEMENTS BY HUNTSMAN

Dismisses and Sets the Record Straight on the Most Blatantly False, Misleading, and Disingenuous Claims from the Company’s Investor Presentation

Believes Management’s Willingness to Mislead its Board and Shareholders Emphasizes the Dire Need for Strong, Capable, and Independent Directors that Are Willing to Hold Management Accountable

Appreciates the Support from Shareholders to Date and Urges All Shareholders to Vote FOR Starboard’s Slate of Highly-Qualified and Experienced Nominees on Starboard’s BLUE Proxy Card TODAY

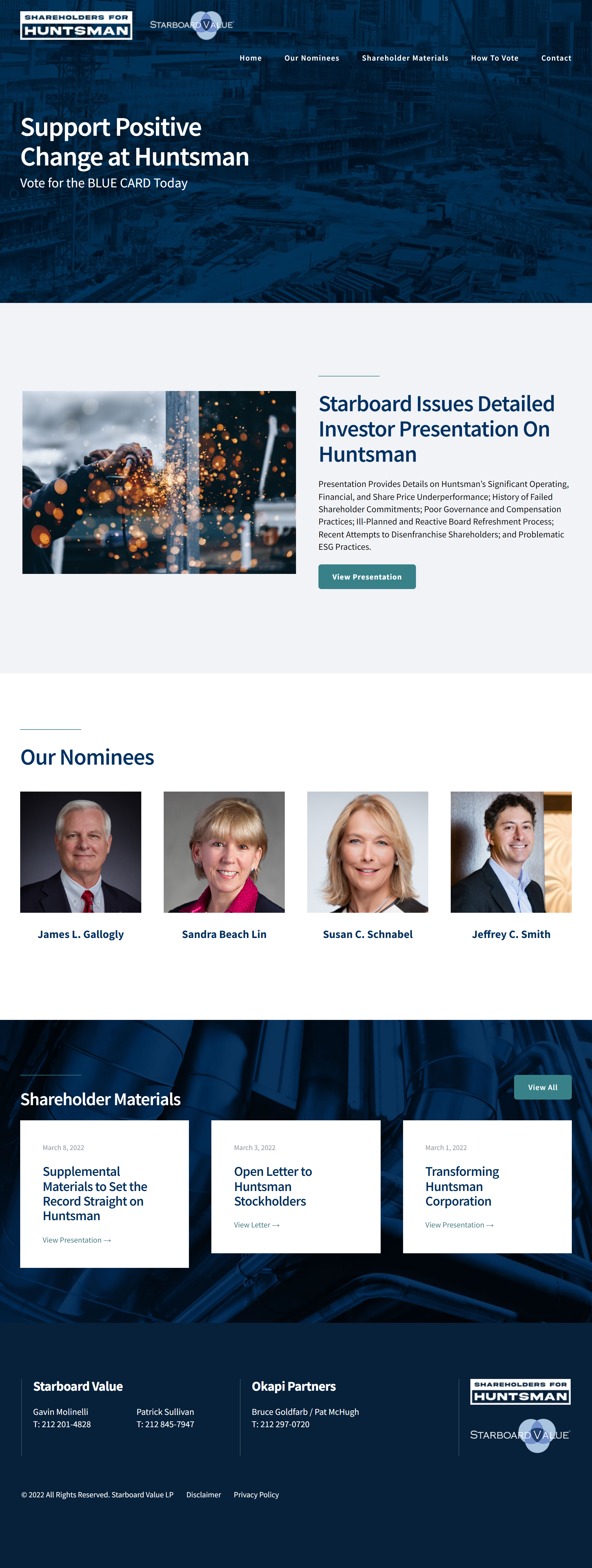

NEW YORK, NY March 8, 2022 /PRNewswire/ -- Starboard Value LP (together with its affiliates, “Starboard” or “we”), one of the largest shareholders of Huntsman Corporation (NYSE: HUN) ("Huntsman," “HUN,” or the "Company"), with an ownership interest of approximately 8.8% of the Company’s outstanding shares, today announced that it has issued a supplemental presentation responding to various false and misleading statements and mischaracterizations made by Huntsman in its recent investor presentation.

The supplemental presentation is available for viewing at https://shareholdersforhuntsman.com/supplemental-materials-to-set-the-record-straight-on-huntsman/

Below are some highlights from Starboard's supplemental presentation.1

| 1. | Huntsman’s troubling history of missed promises and failed commitments to shareholders. |

| · | Reality: Huntsman FAILED to deliver on its 2016 Investor Day target by a substantial margin. |

| o | At its 2016 Investor Day, Huntsman promised shareholders its core business (i.e. ex-TiO2) would reach $1.3 billion of Adjusted EBITDA by 2017. Huntsman then IPO’d its TiO2 business during 2017, leaving it with just the core business, which FAILED to deliver on its $1.3 billion Adjusted EBITDA target. The Company FAILED to deliver on its promise to shareholders, MISSING its target by 11%. |

| o | Huntsman now claims otherwise by asking shareholders to pretend the Company had a different set of assets and a different target in 2017. |

| o | To make its FALSE CLAIM, Huntsman arbitrarily excludes its Chemical Intermediates business, which was a core part of the Company’s portfolio in 2017, from both its Adjusted EBITDA target and its actual results. |

| o | Huntsman is asking shareholders to judge the company using a FICTITIOUS target and MAKE-BELIEVE results. Unsurprisingly, any conclusion reached using Huntsman’s analysis is also MAKE-BELIEVE. |

| o | Do not be fooled. Using real targets based on real results, the Company FAILED to deliver on its 2016 Investor Day promise. |

| · | Reality: Huntsman FAILED to deliver on its promise of growing Adjusted EBITDA organically at a 10% CAGR through 2020. |

| o | At its 2018 Investor Day, Huntsman promised shareholders it would organically grow Adjusted EBITDA at a 10% CAGR through 2020. This would imply a 2020 Adjusted EBITDA target of $1.4 billion – both the Company and Starboard AGREE that this is the target for 2020. |

| o | The Company’s Adjusted EBITDA in 2020 was 52% BELOW its target. Even before the global pandemic in 2020, Wall Street analysts had already expected Huntsman’s 2020 Adjusted EBITDA to be 34% BELOW the $1.4 billion target. Clearly, Huntsman would have FAILED to deliver on its 2018 Investor Day promise. |

| o | Huntsman is now DECEITFULLY claiming to have almost achieved its Adjusted EBITDA target by 2021. Huntsman’s analysis is fundamentally FLAWED, and seems intended to fool shareholders using two tricks. |

| 1. | Huntsman makes a FALSE comparison by comparing a 2020 Adjusted EBITDA target with 2021 actual performance. |

| § | Recall that at its 2018 Investor Day, Huntsman had promised to organically grow Adjusted EBITDA by 10% through 2020. The 2020 target was not a dollar target, it was based on a 10% CAGR. |

1Please refer to the full supplemental presentation available at www.shareholdersforhuntsman.com for additional details, disclosures, supporting data, identity of peers, defined terms, underlying assumptions and other relevant information. The supplemental presentation should also be read in connection with our more comprehensive investor presentation titled “Transforming Huntsman Corporation” available at www.shareholdersforhuntsman.com.

| § | As a result, if one were to try and extend the actual 2020 target to 2021, a proper 2021 comparison should have increased the 2020 target by a further 10%, implying a 2021 Adjusted EBITDA target of $1.5 billion. |

| § | Huntsman’s 2021 actual results are also significantly LOWER than this proper $1.5 billion 2021 target. |

| 2. | Huntsman also INCORRECTLY includes Adjusted EBITDA from M&A in its analysis, despite having explicitly stated at its 2018 Investor Day that its target includes NO M&A and was based ONLY on organic growth. |

| § | When making the proper adjustments, it seems that Huntsman is FALSELY INFLATING its 2021 Adjusted EBITDA by more than $90 million. |

| 3. | Again, we still believe the most intellectually honest assessment would be to use Wall Street analyst unaffected estimates for 2020 results from before the pandemic. Before the global pandemic in 2020, Wall Street analysts had already expected Huntsman’s 2020 Adjusted EBITDA to be 34% BELOW the $1.4 billion target. |

| o | In summary, Huntsman MISSED its 2018 Investor Day target if you looked at it in 2020 AND if you properly looked at it in 2021. Please do not be fooled by the Company’s DISINGENUOUS attempts to retroactively revise its promises and obfuscate the truth. |

| 2. | Huntsman’s poor capital allocation. |

| · | Reality: Huntsman acquired a healthy Textile Effects business in 2006, NOT in 2011 like its shareholder presentation MISLEADINGLY suggests, DESTROYED the business, and the business has only recently recovered to its original state after 16 years. |

| o | Huntsman acquired Textile Effects in 2006 when it had $92 million of Adj. EBITDA, not in 2011 like the Company is conveniently trying to claim. |

| o | The Company PROMISED shareholders that over two years, it would increase Adjusted EBITDA at Textile Effects to $150 million. |

| o | By 2011, just five years later, Huntsman had DESTROYED the business, with Adjusted EBITDA declining from a healthy $92 million to a dismal NEGATIVE $64 million. |

| o | Huntsman is now trying to FOOL shareholders by FALSELY suggesting that Textile Effects had always been a restructuring project. The Company ARBITRARILY selects 2011 as the starting point for its analysis, conveniently ignoring the significant VALUE DESTRUCTION that had occurred over the prior five years. |

| o | The Company and Board should know better as they gave management a special bonus for acquiring this business in 2007. |

| o | Huntsman’s attempt to depict Textile Effects as a turnaround is patently FALSE. Textile Effects was a healthy and profitable business that was expected to increase Adjusted EBITDA to $150 million and never came close. Huntsman very clearly FAILED. Do not be fooled, Textile Effects was NEVER meant to be a turnaround. |

| 3. | Huntsman’s troubling history of poor governance and compensation practices. |

| · | Reality: Huntsman added directors to an entrenched Board but DID NOT REFRESH legacy directors. |

| o | Prior to Starboard’s involvement, Huntsman ONLY ADDED directors to an otherwise entrenched Board. In fact, Huntsman went out of its way to NOT REFRESH interconnected directors by repeatedly waiving mandatory retirement policies. |

| · | Reality: the Company has a FAILING GRADE on pay-for-performance. |

| o | Huntsman cites an ISS report to claim executive pay is aligned with performance, but conveniently omits the rest of the report which shows executive pay is NOT aligned with performance. |

| o | Huntsman’s misleading use of evidence to support an argument that is actually disproved by the very same evidence is incredibly concerning. |

| 4. | Huntsman’s troubling history of financial underperformance. |

| · | Reality: Huntsman’s core reporting segments have not changed meaningfully since its IPO. |

| o | Fifteen years ago, management declared that it had transformed the portfolio and had become a differentiated chemical company. Today, management is again saying the same thing with the same core reporting segments. |

| o | The Company seems to be suggesting that it has only recently become a differentiated chemicals company and so is finally appropriately positioned for commercial and financial success. Do not be fooled! In 2007, fifteen years ago, the Company provided shareholders with the same narrative. |

| o | The Company’s profitability has not meaningfully improved since its IPO and continues to trail the profitability of both Performance and Primary Peers. |

| · | Reality: Huntsman’s Adjusted EBITDA margins remain one of the LOWEST among peers. Huntsman’s margins HAVE NOT been enhanced and have deteriorated from a 500bps deficit to a 900bps deficit relative to peers since its IPO. |

| o | In its latest investor presentation, the Company compares its operating expense ratio to peers while claiming it has undergone “margin enhancement.” Operating expense ratio is not necessarily indicative of profitability. In addition, the Company once again chose an arbitrary peer set in making its comparison. |

| o | The Company’s SG&A expense benchmarking excludes five of its Performance Peers with seemingly no justification, while arbitrarily adding two new companies. |

| o | We believe the Company tried to focus shareholders on its SG&A expense ratio because its profitability is subpar. |

| 5. | Huntsman’s troubling history of share price underperformance. |

| · | Reality: Huntsman DOES NOT have a track record of shareholder value creation and has UNDERPERFORMED both peers and the market across nearly all measurable time periods. |

| o | When compared against Performance Peers, Primary Peers, the broader chemical industry, and even the S&P 500, it seems clear that the Company has FAILED to create shareholder value across almost every time period. |

| o | Huntsman cites five-year TSR as evidence of a “track record of creating shareholder value” but does not justify why five-years is notable, FAILS to analyze any other time period, and selects arbitrary companies as benchmarks, all to fit a narrative seemingly designed to DECEIVE shareholders. |

| o | Across almost EVERY OTHER time period, the Company has significantly underperformed its Performance Peers, Primary Peers, and broader market indices. |

| o | We believe there is NO rationale for why the five-year track record is particularly relevant. Huntsman is benchmarking against a narrow set of companies to fit its narrative. Notably, Huntsman had just exclusively used the S&P 500 as a basis of comparison in a shareholder letter last month. There is no justification provided for why these companies are suddenly better benchmarks as yet another peer group. |

| 6. | Starboard and its slate of highly-qualified, diverse and experienced director nominees. |

| · | Reality: Starboard and its nominees have a proven track record of creating shareholder value, and have extensive and highly relevant expertise in the chemicals industry. |

| · | James L. Gallogly |

| o | Mr. Gallogly’s significant operating, financial, and environmental management experience as a senior executive within the chemicals industry, as well as his significant public company board experience would make him a valuable addition to the Board. |

| o | Mr. Gallogly previously served as a director of E.I. du Pont de Nemours and Company (“DuPont”) from 2015 to 2017. DuPont is one of the largest specialty chemicals companies in the world. Mr. Gallogly has RECENT and SIGNIFICANT experience in the specialty chemicals industry. |

| o | Prior to DuPont, Mr. Gallogly served as Chief Executive Officer and Chairman of the Management Board at LyondellBasell Industries N.V. (“Lyondell”), a global plastics, chemical, and refining company. |

| § | Mr. Gallogly led an impressive turnaround at Lyondell, taking the company from bankruptcy to a best-in-class chemicals company, and generated SUBSTANTIAL VALUE for shareholders, with Lyondell’s TSR outperforming the S&P Chemicals Index by approximately 360% during his tenure. |

| § | In fact, in 2014, while Mr Gallogly was CEO of Lyondell, Peter Huntsman PRAISED Lyondell as having created the GREATEST shareholder value in the chemicals industry over the prior two-and-a-half year period. |

| o | Prior to LyondellBasell, Mr. Gallogly served as Executive Vice President of each major business unit at ConocoPhillips. Prior to ConocoPhillips, Mr. Gallogly served as Chief Executive Officer of Chevron Phillips Chemical Company, a global plastics and chemical company, where he had EXTENSIVE experience managing specialty chemical products and R&D innovation efforts. |

| o | In summary, Mr. Gallogly is among the MOST WELL REGARDED chemicals executives given his long track record of creating substantial shareholder value as both an executive and director. |

| · | Sandra Beach Lin |

| o | Ms. Lin’s significant leadership experience as a senior executive in both the hybrid chemicals and broader industrials industries, coupled with her considerable experience serving on public company boards, would make her a valuable addition to the Board. |

| o | We believe Huntsman has already recognized the value that Ms. Lin would bring to the Board as the Company repeatedly asked her to join the Board during settlement discussions with Starboard earlier this year. |

| o | Ms. Lin has held senior executive positions at Celanese, a global hybrid chemicals company that operates in end markets highly relevant for Huntsman. |

| § | At Celanese, Ms. Lin was previously a Corporate Executive Vice President and President of Advanced Engineered Materials, which is Celanese’s specialty materials business (approximately 50% of Celanese). |

| § | During Ms. Lin’s tenure at Celanese, she led the specialty businesses to a 5x increase in sustainable earnings. |

| o | Ms. Lin was also formerly the President and Chief Executive Officer of Calisolar, a global leader in the production of solar silicon. |

| o | Ms. Lin has also held various senior executive positions at Avery Dennison, Alcoa, and Honeywell International where she gained invaluable specialty materials, sales & marketing, global P&L, and organization realignment skills. |

| o | Ms. Lin currently serves as a director at Avient Corporation, American Electric Power Company, Trinseo S.A., Ripple Therapeutics, and Interface Biologics. At Trinseo S.A., Ms. Lin serves as Chair of the Environmental, Health, Safety, Sustainability and Public Policy Committee, and at American Electric Power Company, Ms. Lin serves as Chair of the Corporate Governance Committee. |

| o | Ms. Lin previously served as a director of WESCO International, Inc. where she oversaw significant shareholder value creation, outperforming the S&P 500 by over 669% during her tenure. |

| o | Ms. Lin has vast operating experience at specialty chemicals and materials companies that are highly relevant to Huntsman. |

| o | Ms. Lin has significant commercial expertise across a wide variety of end-markets that are highly relevant to Huntsman. |

| o | Ms. Lin is a seasoned public company director with immense and relevant experience. |

| · | Susan C. Schnabel |

| o | Ms. Schnabel’s substantial business experience and financial background, coupled with her extensive experience serving as a director of public and private companies, would make her a valuable addition to the Board. |

| o | Ms. Schnabel is the Co-Founder and Co-Managing Partner of aPriori Capital Partners. Previously, Ms. Schnabel served as Managing Director of Credit Suisse Asset Management and Co-Head of DLJ Merchant Banking. Prior to that, Ms. Schnabel served as Chief Financial Officer of PetSmart. |

| o | Ms. Schnabel currently serves as a director of Altice USA, Chair of the Audit Committee of Kayne Anderson BDC, a Trustee of Cornell University, and a director of various other university and non-profit Boards of Directors. |

| o | Ms. Schnabel previously served as a director of Versum Materials (“VSM”), STR Holdings, Neiman Marcus, Pinnacle Gas Resources, Rockwood Holdings, Shoppers Drug Mart Corporation (TSX), and other private company Boards of Directors. |

| o | Ms. Schnabel is a chemical engineer by background, has had a highly successful career as a private equity investor, and is a seasoned public board member with a deep understanding of governance best practices. |

| o | From October 2016 to October 2019, Ms. Schnabel served as a member of VSM’s |

Board of Directors. VSM was a specialty electronic chemicals company, and meaningfully outperformed both the S&P Chemicals and the broader market indices during her tenure on the Board.

| o | Ms. Schnabel was a key investor and board member during the transformative stages of Rockwood Holdings, a specialty chemicals company. Rockwood was ultimately sold to Albemarle, generating highly attractive returns for all shareholders. |

| · | Jeffrey C. Smith |

| o | Mr. Smith’s extensive knowledge of the capital markets, corporate finance, and public company governance practices, together with his significant public company board experience, would make him a valuable addition to the Board. |

| o | Mr. Smith is a Managing Member, Chief Executive Officer, and Chief Investment Officer of Starboard Value. |

| o | Mr. Smith currently serves as Chair of the Board of Directors of Papa John’s International, and as a director of Cyxtera Technologies. |

| o | Mr. Smith previously served as Chair of the Board of Directors of Advance Auto Parts, Darden Restaurants, and Phoenix Technologies. In addition, Mr. Smith has also served as a director of many other public companies. |

| o | Mr. Smith is a highly experienced public company director having served on numerous boards in the past, including as Chair on five separate occasions. |

| o | Mr. Smith joined the Board of Papa Johns as Chair in February 2019. Since then, Papa John’s has substantially outperformed the S&P 500. |

PLEASE DO NOT BE FOOLED BY HUNTSMAN’S MANY MISLEADING, REVISIONIST, AND DISINGENUOUS CLAIMS! HUNTSMAN NEEDS STRONG INDEPENDENT BOARD MEMBERS WHO WILL DEMAND ACCOUNTABILITY.

If management is willing to mislead shareholders, we believe management may also be willing to mislead the Board, further emphasizing the dire need for change in the boardroom. Huntsman NEEDS directors that are experienced and independent enough to hold management accountable. Our strong, capable, and independent director nominees WILL NOT BE FOOLED by Huntsman’s disingenuous tactics.

VOTE FOR CHANGE ON THE BLUE PROXY CARD TODAY

Please support our efforts to revitalize Huntsman by voting on the BLUE proxy card to elect our slate of highly qualified nominees at the Company’s upcoming 2022 Annual Meeting of Shareholders.

Our detailed presentation and other important information and materials regarding the Annual Meeting can be viewed at www.shareholdersforhuntsman.com.

If you have any questions or need further assistance with voting your Huntsman shares, please contact Okapi Partners LLC at the phone numbers or email listed below.

Shareholders may call toll-free: (877) 629-6356

Banks and brokers call: (212) 297-0720

E-mail: info@okapipartners.com

About Starboard Value LP

Starboard Value LP is a New York-based investment adviser with a focused and differentiated fundamental approach to investing primarily in publicly traded U.S. companies. Starboard seeks to invest in deeply undervalued companies and actively engage with management teams and boards of directors to identify and execute on opportunities to unlock value for the benefit of all shareholders.

Investor contacts:

Gavin Molinelli, (212) 201-4828

Patrick Sullivan, (212) 845-7947

www.starboardvalue.com

Okapi Partners

Bruce H. Goldfarb/Patrick McHugh

(212) 297-0720

Item 3: On March 8, 2022, Starboard uploaded the following materials to www.shareholdersforhuntsman.com: