Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on November 24, 2004

Registration No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Huntsman Corporation

(Exact Name of Registrant as Specified in its Charter)

| Delaware (State or Other Jurisdiction of Incorporation or Organization) |

2800 (Primary Standard Industrial Classification Code Number) |

42-1648585 (I.R.S. Employer Identification Number) |

||

500 Huntsman Way Salt Lake City, UT 84108 (801) 584-5700 (Address, Including Zip Code and Telephone Number, Including Area Code, of Registrant's Principal Executive Offices) |

||||

Samuel D. Scruggs

Executive Vice President, General Counsel and Secretary

Huntsman Corporation

500 Huntsman Way

Salt Lake City, UT 84108

(801) 584-5700

(Name, Address, Including Zip Code, and Telephone

Number, Including Area Code, of Agent For Service)

| Copies to: | ||

| Jeffery B. Floyd Vinson & Elkins L.L.P. 1001 Fannin, Suite 2300 Houston, TX 77002 (713) 758-2222 |

Gregory A. Fernicola Skadden, Arps, Slate, Meagher & Flom LLP Four Times Square New York, NY 10036 (212) 735-3000 |

|

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: o

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box: o

CALCULATION OF REGISTRATION FEE

| Title of Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1) |

Amount of Registration Fee |

||||

|---|---|---|---|---|---|---|

| Common Stock, $0.01 par value | $ | 1,610,000,000 | $ | 203,987 | ||

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment that specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED NOVEMBER 24, 2004

P R O S P E C T U S

Huntsman Corporation

Shares

Common Stock

This is an initial public offering of our common stock. We currently expect the initial public offering price to be between $ and $ per share. We have applied to have the common stock listed on the New York Stock Exchange under the symbol "HUN."

We are selling shares of common stock and the selling stockholder named in this prospectus is selling shares. The shares being sold by the selling stockholder will represent less than 10% of the aggregate number of shares being sold in this offering. We will not receive any proceeds from the sale of shares by the selling stockholder.

We and the selling stockholder have granted the underwriters an option to purchase up to additional shares of common stock to cover over-allotments.

Investing in our common stock involves risks. See "Risk Factors" on page 15.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| |

Per Share |

Total |

||||

|---|---|---|---|---|---|---|

| Public Offering Price | $ | $ | ||||

| Underwriting Discount | $ | $ | ||||

| Proceeds to Huntsman Corporation (before expenses) | $ | $ | ||||

| Proceeds to the selling stockholder (before expenses) | $ | $ | ||||

The Underwriters expect to deliver the shares to purchasers on or about , 2004.

| Citigroup |

Credit Suisse First Boston |

Merrill Lynch & Co. |

Deutsche Bank Securities |

The date of this prospectus is , 2004.

Until , 2005 (25 days after the date of this prospectus), all dealers that buy, sell or trade our common stock, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers' obligation to deliver a prospectus when acting as underwriters and with respect to unsold allotments or subscriptions.

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not making an offer of these securities in any jurisdiction where the offer is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than the date on the front of this prospectus.

Industry and Market Data

This prospectus includes information with respect to market share, industry conditions and forecasts that we obtained from internal industry research, publicly available information (including industry publications and surveys), and surveys and market research provided by consultants (including Nexant, Inc., an international consulting and research firm ("Nexant"), Chemical Market Associates, Inc., an international consulting and research firm ("CMAI"), International Business Management Associates, an industry research and consulting firm ("IBMA"), and others). The publicly available information and the reports, forecasts and other research provided by consultants generally state that the information contained therein has been obtained from sources believed to be reliable, but there can be no assurance as to the accuracy and completeness of such information. We have not independently verified any of the data from third-party sources, nor have we ascertained the underlying economic assumptions relied upon therein. Similarly, our internal research and forecasts are based upon our management's understanding of industry conditions, and such information has not been verified by any independent sources. As is noted, certain statements in this prospectus are based on information provided by consultants that we commissioned to provide us with the referenced information.

i

The following summary highlights selected information from this prospectus and does not contain all of the information that you should consider before investing in our common stock. This prospectus contains information regarding our businesses and detailed financial information. You should carefully read this entire prospectus, including the historical and pro forma financial statements and related notes, before making an investment decision.

Huntsman Corporation is a new company formed to hold the existing businesses of Huntsman Holdings, LLC. Concurrently with the consummation of this offering, Huntsman Holdings, LLC will be merged into Huntsman Corporation in a transaction we refer to as the "Reorganization Transaction." The pro forma and pro forma as adjusted financial data included in this prospectus give effect to the transactions described in "Unaudited Pro Forma Financial Data."

In this prospectus, "Huntsman Corporation," the "company," "we," "us" or "our" refer to Huntsman Corporation and its subsidiaries, including our predecessor Huntsman Holdings, LLC after giving effect to the Reorganization Transaction, except where the context makes clear that the reference is only to Huntsman Corporation itself and not its subsidiaries. Huntsman Holdings, LLC has conducted its operations through three principal subsidiaries: Huntsman LLC, Huntsman International Holdings LLC and Huntsman Advanced Materials LLC. In this prospectus, the term "HLLC" refers to Huntsman LLC and, unless the context otherwise requires, its subsidiaries, the term "HIH" refers to Huntsman International Holdings LLC and, unless the context otherwise requires, its subsidiaries, and the term "Advanced Materials" refers to Huntsman Advanced Materials LLC and, unless the context otherwise requires, its subsidiaries. A glossary of chemical abbreviations used in this prospectus begins on page 166.

Overview

We are among the world's largest global manufacturers of differentiated and commodity chemical products. We manufacture a broad range of chemical products and formulations, which we market in more than 100 countries to a diversified group of consumer and industrial customers. Our products are used in a wide range of applications, including those in the adhesives, aerospace, automotive, construction products, durable and non-durable consumer products, electronics, medical, packaging, paints and coatings, power generation, refining and synthetic fiber industries. We are a leading global producer in many of our key product lines, including MDI, amines, surfactants, epoxy- based polymer formulations, maleic anhydride and titanium dioxide. We operate 63 manufacturing facilities located in 22 countries and employ over 11,500 associates. Our businesses benefit from significant vertical integration, large production scale and proprietary manufacturing technologies, which allow us to maintain a low-cost position. We had pro forma revenues for the nine months ended September 30, 2004 and the year ended December 31, 2003 of $8.4 billion and $9.3 billion, respectively.

Our Products and Segments

Our business is organized around our six segments: Polyurethanes, Advanced Materials, Performance Products, Pigments, Polymers and Base Chemicals. These segments can be divided into two broad categories: differentiated and commodity. We produce differentiated products primarily in our Polyurethanes, Advanced Materials and Performance Products segments. These products serve diverse end markets and are generally characterized by historical growth in excess of GDP growth resulting from product substitution and new product development, proprietary manufacturing processes and product formulations and a high degree of customer loyalty. Demand for these products tends to be driven by the value-added attributes that they create in our customers' end-use applications. While the demand for these differentiated products is also influenced by worldwide economic conditions and GDP growth, our differentiated products have tended to produce more stable profit margins and higher demand growth rates than our commodity products.

1

In our commodity chemical businesses, we produce titanium dioxide derived from titanium-bearing ores in our Pigments segment and petrochemical-based olefins, aromatics and polyolefins products in our Polymers and Base Chemicals segments. Since the coatings industry consumes a substantial portion of titanium dioxide production, seasonal demand patterns in the coatings industry drive the profitability of our Pigments segment. The profitability of our petrochemical-based commodity products is cyclical and has been experiencing a down cycle for the last several years, resulting primarily from significant new capacity additions, a decrease in demand reflecting weak global economic conditions and high raw material costs. Certain industry fundamentals have recently improved and, according to Nexant and IBMA, point to increased profitability in the markets for the major commodity products that we manufacture.

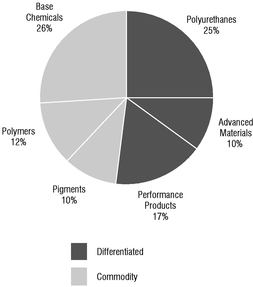

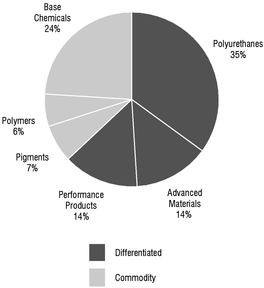

The following charts set forth information regarding the revenues and EBITDA of our six business segments for the nine months ended September 30, 2004:

| Segment Revenues* |

Segment EBITDA* |

|

|---|---|---|

|

|

2

The following table identifies the key products, their principal end markets and applications and representative customers of each of our segments:

| Segment |

Products |

End Markets and Applications |

Representative Customers |

|||

|---|---|---|---|---|---|---|

| Polyurethanes | MDI, PO, polyols, PG, TDI, TPU, aniline and MTBE | automotive interiors, refrigeration and appliance insulation, construction products, footwear, furniture cushioning, adhesives, specialized engineering applications and fuel additives | BMW, Collins & Aikman, Electrolux, Firestone, Lear, Louisiana Pacific, Shell, Weyerhauser | |||

Advanced Materials |

epoxy resin compounds and formulations; cross-linking, matting and curing agents; epoxy, acrylic and polyurethane-based adhesives and tooling resin formulations |

adhesives, aerospace, electrical power transmission, consumer electronics, civil engineering, wind power generation and automotive |

ABB, Akzo, BASF, Boeing, Bosch, Cytec, Hexcel, Rohm & Haas, Sherwin Williams |

|||

Performance Products |

ethyleneamines, ethanolamines, polyetheramines, carbonates, surfactants, LAB, maleic anhydride, EO and EG |

detergents, personal care products, agrochemicals, lubricant and fuel additives, paints and coatings, construction, marine and automotive products and PET fibers and resins |

ChevronTexaco, Colgate, Ecolab, Henkel, Monsanto, Procter & Gamble, Unilever |

|||

Pigments |

titanium dioxide |

paints and coatings, plastics, paper, printing inks, fibers and ceramics |

Akzo, Atofina, Clariant, ICI, Jotun, PolyOne |

|||

Polymers |

LDPE and LLDPE, polypropylene, EPS, styrene and APAO |

flexible and rigid packaging, adhesives and automotive, medical and construction products |

Ashland, Kerr, Kimberly Clark, Pliant, Polymer Group, PolyOne, Sealed Air |

|||

Base Chemicals |

ethylene, propylene, butadiene, benzene, cyclohexane, paraxylene and MTBE |

packaging film, polyester and nylon fibers, PVC, cleaning compounds, polymer resins, SBR rubber and fuel additives |

Bayer, BP, Bridgestone/Firestone, Dow, DuPontSA, Invista, Goodyear, Nova, Shell, Solvay |

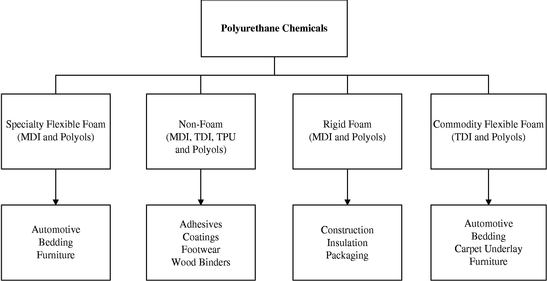

Polyurethanes

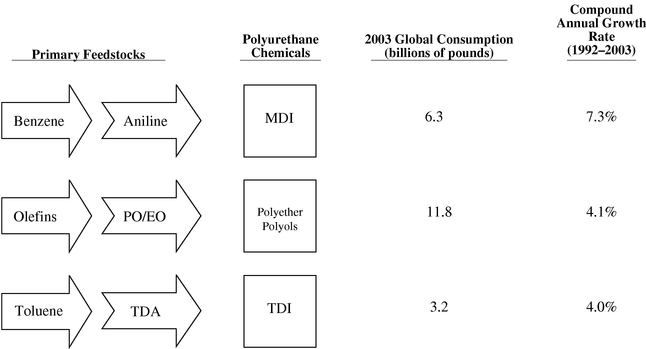

We are a leading global manufacturer and marketer of a broad range of polyurethane chemicals, including MDI, PO, polyols, PG, TDI and TPU. Polyurethane chemicals are used to produce rigid and flexible foams, as well as coatings, adhesives, sealants and elastomers. We focus on the higher-margin, higher-growth markets for MDI and MDI-based polyurethane systems. Growth in our Polyurethanes

3

segment has been driven primarily by the continued substitution of MDI-based products for other materials across a broad range of applications. As a result, according to Nexant, global consumption of MDI grew at a compound annual growth rate of 7.3% from 1992 to 2003. Our Polyurethanes segment is widely recognized as an industry leader in utilizing state-of-the-art application technology to develop new polyurethane systems and applications. In 2003 approximately 20% of the revenues from our MDI-based products were generated from products and applications introduced in the previous three years. According to Nexant, we are the lowest-cost and second-largest producer of MDI in the world. We operate four primary Polyurethanes manufacturing facilities in the U.S. and Europe. We also operate 14 Polyurethanes formulation facilities, which are located in close proximity to our customers worldwide. We have a significant interest in a manufacturing joint venture that has recently begun construction of a low-cost, world-scale, integrated MDI production facility near Shanghai, China. We expect production at this facility to commence in 2006.

Advanced Materials

We are a leading global manufacturer and marketer of technologically advanced epoxy, acrylic and polyurethane-based polymer products. We focus on formulations and systems that are used to address customer-specific needs in a wide variety of industrial and consumer applications. Our products are used either as replacements for traditional materials such as metal, wood, clay, glass, stone and ceramics, or in applications where traditional materials do not meet demanding engineering specifications. For example, structural adhesives are used to replace metal rivets and advanced composites are used to replace traditional aluminum panels in the manufacture of aerospace components. Revenue growth for much of our product portfolio has historically been well in excess of global GDP growth. Our Advanced Materials segment is characterized by the breadth of our product offering, our expertise in complex chemistry, our long-standing relationships with our customers and our ability to develop and adapt our technology and our applications expertise for new markets and new applications. We market over 6,000 products to more than 5,000 customers. We operate 15 Advanced Materials synthesis and formulating facilities in North America, Europe, Asia, South America and Africa.

Performance Products

Our Performance Products segment is organized around three business groups, performance specialties, performance intermediates, and maleic anhydride and licensing, and serves a wide variety of consumer and industrial end markets. In performance specialties, we are a leading global producer of amines, carbonates and certain specialty surfactants. Growth in demand in our performance specialties business tends to be driven by the end-performance characteristics that our products deliver to our customers. These products are manufactured for use in a growing number of niche industrial end uses and have been characterized by growing demand and stable profitability. For example, we are one of two significant global producers of polyetheramines, for which our sales volumes have grown at a compound annual rate of over 13% in the last ten years due to strong demand in a number of industrial applications, such as epoxy curing agents, fuel additives and civil construction materials. In performance intermediates, we consume internally produced and third-party-sourced base petrochemicals in the manufacture of our surfactants, LAB and ethanolamines products, which are primarily used in detergent and consumer products applications. We also produce EG, which is primarily used in the production of polyester fibers and PET packaging, and EO, all of which is consumed internally in the production of our downstream products. We believe we are North America's largest and lowest-cost producer of maleic anhydride. Maleic anhydride is the building block for UPRs, mainly used in the production of fiberglass reinforced resins for marine, automotive and construction products. We are the leading global licensor of maleic anhydride manufacturing technology and are also the largest supplier of a catalyst used in the manufacture of maleic anhydride. We operate 16 Performance Products manufacturing facilities in North America, Europe and Australia.

4

Pigments

We are a leading global manufacturer and marketer of titanium dioxide, which is a white pigment used to impart whiteness, brightness and opacity to products such as paints, plastics, paper, printing inks, fibers and ceramics. According to IBMA, our Pigments segment, which operates under the trade name "Tioxide®," is the fourth largest producer of titanium dioxide in the world, with an estimated 12% of global production capacity, and the largest producer of titanium dioxide in Western Europe, with an estimated 23% of Western European production capacity. The global titanium dioxide market is characterized by a small number of large, global producers. We operate eight chloride-based and sulfate-based titanium dioxide manufacturing facilities located in North America, Europe, Asia and Africa.

Polymers

We manufacture and market polypropylene, polyethylene, EPS, EPS packaging and APAO. We consume internally produced and third-party-sourced base petrochemicals, including ethylene and propylene, as our primary raw materials in the manufacture of these products. In our polyethylene, APAO and certain of our polypropylene product lines, we pursue a targeted marketing strategy by focusing on those customers and end use applications that require customized polymer formulations. We produce these products at our smaller and more flexible Polymers manufacturing facilities and generally sell them at premium prices. In our other product lines, including the balance of our polypropylene, EPS and EPS packaging, we maintain leading regional market positions and operate cost-competitive manufacturing facilities. We operate six primary Polymers manufacturing facilities in North America and Australia. We are expanding the geographic scope of our polyethylene business and improving the integration of our European Base Chemicals business through the construction of an integrated, low-cost, world-scale LDPE plant to be located adjacent to our existing olefins facility in Wilton, U.K. Upon completion of this facility, which we expect will occur in late 2007, we will consume approximately 50% of the output from our U.K. ethylene unit in the production of LDPE.

Base Chemicals

We are a highly integrated North American and European producer of olefins and aromatics. We consume a substantial portion of our Base Chemicals products, such as ethylene, propylene and benzene, in our Performance Products and Polyurethanes segments. We believe this integration leads to higher operating rates for our Base Chemical assets, improved reliability of raw material supply for our other segments and reduced logistics and transportation costs. We operate four Base Chemicals manufacturing facilities located on the Texas Gulf Coast and in northeast England. These facilities are equipped to process a variety of oil- and natural gas-based feedstocks and benefit from their close proximity to multiple sources of these raw materials. This flexibility allows us to optimize our operating costs. These facilities also benefit from extensive underground storage capacity and logistics infrastructure, including pipelines, deepwater jetties and ethylene liquefaction facilities.

Current Industry Conditions

Over the past several years, the global chemical industry has generally experienced depressed market conditions due to weak demand, lower capacity utilization rates and high, volatile feedstock costs. In 2004, the profitability of the industry has generally improved as demand has recovered and additions of new manufacturing capacity have been limited.

Growth in our Polyurethanes and Advanced Materials segments has been driven by the continued substitution of our products for other materials across a broad range of applications as well as the level of global economic activity. Historically, demand for many of these products has grown at rates in excess of GDP growth. In Polyurethanes, this growth, particularly in Asia, has recently resulted in

5

improved demand and higher industry capacity utilization rates for many of our key products, including MDI. In 2004, the profitability of our Polyurethanes and Advanced Materials segments has improved due to increased demand in several of our key industrial end markets, including aerospace, automotive and construction products. This has allowed us to increase selling prices, which has more than offset increases in the cost of our primary raw materials, including benzene, propylene and chlorine.

In our Performance Products segment, demand for our performance specialties has generally continued to grow at rates in excess of GDP as overall demand is significantly influenced by new product and application development. In 2004, overall demand for most of our performance intermediates has generally been stable or improving, but excess surfactant manufacturing capacity in Europe and a decline in the use of LAB in new detergent formulations has limited our ability to increase prices in response to higher raw material costs. In EG, higher industry capacity utilization rates in 2004 due to stronger demand in the PET resin and Asian fiber markets have resulted in higher profitability.

Our Pigments segment experienced difficult business conditions throughout 2003 and much of 2004, reflecting soft economic conditions, but industry fundamentals have recently strengthened. This has resulted in higher capacity utilization rates and improved product pricing. The cost of titanium-bearing ores, which is the primary raw material used to produce titanium dioxide, has been relatively stable. IBMA currently expects that titanium dioxide industry operating rates will continue to increase as a result of increased demand from improving economic conditions and a lack of significant new planned capacity additions.

The profitability of our Polymers and Base Chemicals segments has historically been cyclical. The industry has recently operated in a down cycle that resulted from significant new capacity additions, weak demand reflecting soft global economic conditions and high crude oil and natural gas-based raw material costs. Despite continued high feedstock costs, the profitability of our Base Chemicals segment has improved in 2004 as demand has strengthened and average selling prices and profit margins have increased in most of our product lines. Limited new capacity additions have been announced for these products in North America and Western Europe over the next several years. Consequently, Nexant currently expects operating rates and profit margins in the polymers and base chemicals markets to increase as demand continues to recover as a result of improved global economic conditions.

Competitive Strengths

Leading Market Positions in Our Differentiated Product Segments

We derive a substantial portion of our revenues and EBITDA from our Polyurethanes, Advanced Materials and Performance Products segments, which manufacture our differentiated products. For the nine months ended September 30, 2004, these segments accounted for 52% of our revenues and 63% of our segment EBITDA, as described on page 2. We enjoy leading market positions in many of our primary product lines in these segments, including MDI, amines, carbonates, specialty surfactants, maleic anhydride, adhesives and epoxy-based polymer formulations. Demand for many of these products has been relatively resistant to changes in global economic conditions and has historically grown at rates in excess of GDP growth due to new product development and the continued substitution of our products for traditional materials and chemicals. We produce many of these products using our proprietary manufacturing processes, and we own many patents related to our processes, product formulations and their end-use applications. The markets for many of these products also benefit from a limited number of global producers, significant barriers to entry and a high degree of customer loyalty.

6

Large Scale, Integrated Manufacturer with Low Cost Operations

We are among the world's largest global manufacturers of chemical products. We operate 63 manufacturing facilities located in 22 countries as well as numerous sales, technical service and research facilities. We believe that the scale of our operations enables us to source raw materials and services that we purchase from third parties on terms more advantageous than those available to our smaller competitors. In addition, we are able to leverage selling, administrative and corporate overhead service platforms in order to reduce the operating costs of our businesses, including those that we have acquired. Our scale has also allowed us to rationalize smaller, less efficient capacity in recent years.

Our businesses also benefit from significant product integration. In 2003, we utilized approximately half of our ethylene production and all our EO production in the manufacturing operations of our Performance Products and Polymers segments. In addition, we utilized substantially all the benzene that we produced in the production of our aromatics and MDI. We believe that our high degree of product integration provides us with a competitive advantage over non-integrated producers by reducing both our exposure to cyclical raw material prices and our raw material transportation costs, as well as increasing the operating rates of our facilities. We believe our large production scale and integration enable us to manufacture and market our products at costs that are lower than those achieved by smaller, less integrated producers.

Diverse Customer Base Across Broad Geographic Regions

We sell our products to a highly diverse base of customers who are located in all major geographic regions and represent many end-use industry groups. We have thousands of customers in more than 100 countries. We have developed a global presence, with approximately 47% of our pro forma revenues for the year ended December 31, 2003 from North America, approximately 37% from Europe, approximately 12% from the Asia/Pacific region and approximately 4% from South America and other regions. We believe that this diversity limits our dependence on any particular product line, customer, end market or geographic region.

Experienced Management

We are managed by an experienced group of executives, led by Jon M. Huntsman, our Chairman of the Board, and Peter R. Huntsman, our President and Chief Executive Officer. Jon M. Huntsman is the founder of our company and has over 40 years of experience in the chemicals and plastics industries. Peter Huntsman has over 20 years of experience in the chemicals and plastics industries. Both have been instrumental in leading our company through periods of growth and industry cycles. The balance of our executive management team has extensive industry experience and prior work experience at leading chemical and professional services firms, including Imperial Chemical Industries PLC, Texaco, Inc., Mobil Corporation, Bankers Trust Company and Skadden, Arps, Slate, Meagher & Flom LLP. Throughout our history, our management team has demonstrated expertise and entrepreneurial spirit in expanding our businesses, integrating numerous acquisitions and executing on significant cost cutting programs.

Business Strategy

Expand Our Differentiated Segments

Since 1999, we have invested over $500 million in discretionary capital expenditures and completed seven strategic acquisitions to expand our differentiated segments. As a result, for the nine months ended September 30, 2004, these segments produced 52% of our revenues and 63% of our segment EBITDA. We intend to continue to invest our capital in our higher-growth, higher-margin differentiated segments in order to expand the breadth of our product offerings, extend the geographic scope of these businesses and increase our production capacity to meet growing customer demand. As

7

part of this strategy, we have a significant interest in a manufacturing joint venture that has recently begun construction of a world-scale MDI production facility near Shanghai, China. We believe that this will enable us to strengthen our long-standing presence in China and to further capitalize on the growth in demand for MDI in Asia. We intend to continue to invest in our global research and development capabilities in order to meet the increasingly sophisticated needs of our customers in areas of new product development and product application technology. We have recently announced that we will consolidate substantially all of our existing North American Polyurethanes, Advanced Materials and Performance Products research and development, technical service and process technology capabilities in a new, state-of-the-art facility to be constructed in The Woodlands, Texas.

Maximize Cash Generated By Our Commodity Segments

We derived 48% of our revenues and 37% of our segment EBITDA for the nine months ended September 30, 2004 from our Pigments, Polymers and Base Chemicals segments. We believe we have cost-competitive facilities in each of these segments, which produce primarily commodity products. In periods of favorable market conditions, our commodity businesses have historically generated significant amounts of free cash flow. We intend to continue to selectively invest sufficient capital to sustain the competitive position of our existing commodity facilities and improve their cost structure. In addition, we intend to capitalize on the low-cost position of our Wilton, U.K. olefins facility by constructing a world-scale LDPE facility on an adjacent site.

Continue Focus on Improving Operational Efficiencies

We continuously focus on identifying opportunities to reduce our operating costs and maximize our operating efficiency. We have completed a number of targeted cost reduction programs and other actions since 1999. These programs have included, among other things, the closing of seven high-cost manufacturing units as well as reducing corporate and administrative costs. More recently, we have announced a comprehensive global cost reduction program, which we refer to as "Project Coronado," with a goal of further reducing our annual fixed manufacturing and selling, general and administrative costs by $200 million by 2006. In connection with Project Coronado, we have recently announced the closure of eight smaller, less competitive manufacturing units in our Polyurethanes, Advanced Materials, Performance Products and Pigments segments. These and other actions have resulted in the reduction of approximately 1,500 employees in these businesses since 2000.

Further Reduce Our Indebtedness

We intend to use substantially all of our net proceeds from this offering to reduce our outstanding indebtedness. This will result in a significant reduction in our annual interest expense. If the profitability of our businesses continues to improve, we intend to further reduce the level of our indebtedness.

Our History

Jon M. Huntsman founded the predecessor to our company in the early 1970s as a small packaging company. Since then, we have grown through a series of significant acquisitions and now own a global portfolio of commodity and differentiated businesses. In 1993, we purchased the LAB and maleic anhydride businesses of The Monsanto Company. In 1994, we purchased the global chemical business from what was formerly Texaco Inc. In 1997, we purchased our PO business from Texaco. Also in 1997, we acquired Rexene Corporation, significantly increasing the size of our Polymers business. In 1999, we acquired certain polyurethanes, pigments and European petrochemicals businesses from Imperial Chemical Industries PLC ("ICI"). In 2000, we completed the acquisition of the Morton global TPU business from The Rohm and Haas Company. In 2001, we completed our acquisition of the global ethyleneamines business of Dow Chemical Company, and we completed our acquisition of the

8

Albright & Wilson European surfactants business from Rhodia S.A. In 2003, we completed our acquisition of 88% of our Advanced Materials business through the purchase of Vantico Group S.A., and we now own approximately 90% of Advanced Materials.

We have also divested certain non-core businesses, including our packaging subsidiary in 1997 and our global styrenics business in 1998.

The Reorganization Transaction

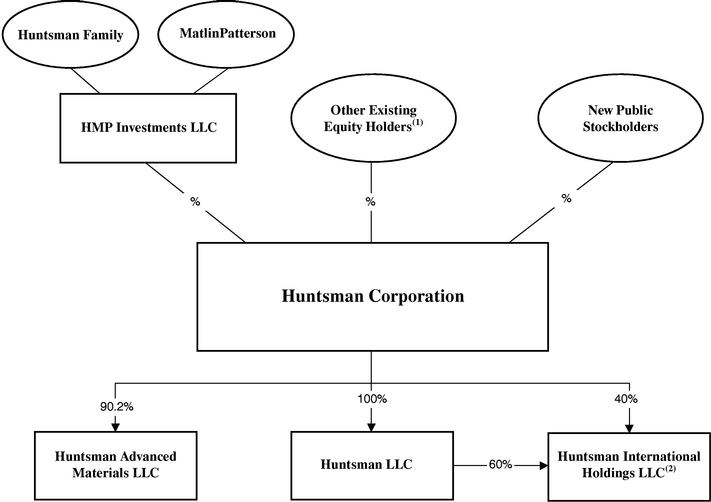

We will consummate the Reorganization Transaction in connection with the completion of this offering. In the Reorganization Transaction, Huntsman Holdings, LLC will merge into us, and the existing holders of the common and preferred membership interests of Huntsman Holdings, LLC, including the mandatorily redeemable preferred interests, will receive, directly or indirectly, shares of our common stock in exchange for their interests. In addition, the holders of warrants in our subsidiary HMP Equity Holdings Corporation ("HMP") will exchange all of their warrants for shares of our common stock. Immediately prior to the merger, Huntsman Family Holdings Company LLC ("Huntsman Family Holdings"), which is owned by Jon M. Huntsman and certain members of his family, and MatlinPatterson Global Opportunities Partners L.P., MatlinPatterson Global Opportunities B, L.P. and MatlinPatterson Global Oportunities (Bermuda), L.P. (collectively, "MatlinPatterson") will contribute all of their membership interests in Huntsman Holdings, LLC to HMP Investments LLC, a new entity formed to hold such interests ("Investments LLC"). Investments LLC will receive shares of our common stock in exchange for these interests. Huntsman Family Holdings will control Investments LLC, including the voting of the shares of our common stock held by Investments LLC. However, Investments LLC will not be able to vote its shares of our common stock in favor of certain corporate actions without the consent of MatlinPatterson. MatlinPatterson will have control over the disposition of the shares of our common stock held by Investments LLC that are allocated to MatlinPatterson's membership interests in Investments LLC. In addition, Huntsman Family Holdings has agreed to cause all of the shares of our common stock held by Investments LLC to be voted in favor of the election to our board of directors of two nominees designated by MatlinPatterson. Immediately following the Reorganization Transaction and this offering, Investments LLC will hold a majority of our outstanding common stock.

9

The following chart reflects our organizational structure immediately after the completion of this offering.

10

The Offering

| Issuer | Huntsman Corporation | |

Common stock offered by us |

shares |

|

Common stock offered by the selling stockholder |

shares |

|

Common stock to be outstanding after this offering |

shares |

|

Use of Proceeds |

We estimate that the net proceeds to us from the offering will be approximately $1,250 million. We intend to use these net proceeds for the repayment of outstanding indebtedness and for general corporate purposes. |

|

We will not receive any of the proceeds from the sale of shares by the selling stockholder. See "Use of Proceeds." |

||

Proposed New York Stock Exchange Symbol |

HUN |

|

Risk Factors |

This offering involves risks. See "Risk Factors" on page 15. |

Unless we specifically state otherwise, all information in this prospectus:

Our principal executive offices are located at 500 Huntsman Way, Salt Lake City, Utah 84108, and our telephone number is (801) 584-5700.

11

SUMMARY HISTORICAL AND PRO FORMA AS ADJUSTED FINANCIAL DATA

The summary historical financial data set forth below presents the historical financial data of our predecessor Huntsman Holdings, LLC. In such financial data, HIH is accounted for using the equity method of accounting through April 30, 2003. Effective May 1, 2003, as a result of the HIH Consolidation Transaction (as defined below), we have consolidated the financial results of HIH. Effective July 1, 2003, as a result of the AdMat Transaction (as defined below), we have consolidated the financial results of Advanced Materials. As a result, the financial information as of and for the year ended December 31, 2003 is not comparable to the prior years' historical financial data presented herein, and the financial information as of and for the nine months ended September 30, 2004 is not comparable to the financial information as of and for the nine months ended September 30, 2003.

In order to present data that is useful for comparative purposes, we have provided pro forma as adjusted statement of operations data for the year ended December 31, 2003 and the nine months ended September 30, 2003 and 2004, which gives pro forma effect to the following transactions as if each transaction had occurred on January 1, 2003:

and which is adjusted to give effect to the following transactions as if each transaction had occurred on January 1, 2003:

We have also provided pro forma as adjusted balance sheet data which gives effect to the following transactions as if each transaction had occurred on September 30, 2004:

The unaudited pro forma as adjusted financial data does not purport to be indicative of the combined financial position or results of operations of future periods or indicative of results that would have occurred had the above transactions been completed on the dates indicated.

The summary financial data set forth below should be read in conjunction with the Consolidated Financial Statements, "Management's Discussion and Analysis of Financial Condition and Results of

12

Operations," "Unaudited Pro Forma Financial Data," and "Selected Historical Financial Data" included elsewhere in this prospectus and, in each case, the notes related thereto.

| |

Year Ended December 31, |

Nine Months Ended September 30, |

|||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

|

|

|

Pro Forma As Adjusted |

|

|

Pro Forma As Adjusted |

||||||||||||||||||

| |

2001 |

2002 |

2003 |

2003(a) |

2003 |

2004 |

2003(a) |

2004(a) |

|||||||||||||||||

| |

(in millions) |

||||||||||||||||||||||||

| Statement of Operations Data: | |||||||||||||||||||||||||

| Revenues | $ | 2,757.4 | $ | 2,661.0 | $ | 7,080.9 | $ | 9,252.4 | $ | 4,711.1 | $ | 8,357.7 | $ | 6,885.2 | $ | 8,357.7 | |||||||||

| Cost of goods sold | 2,666.6 | 2,421.0 | 6,373.1 | 8,255.1 | 4,258.7 | 7,358.0 | 6,150.1 | 7,358.0 | |||||||||||||||||

| Gross profit | 90.8 | 240.0 | 707.8 | 997.3 | 452.4 | 999.7 | 735.1 | 999.7 | |||||||||||||||||

| Operating expenses | 211.7 | 174.7 | 493.4 | 732.2 | 333.3 | 580.9 | 567.2 | 580.9 | |||||||||||||||||

| Restructuring, impairment and plant closing costs (credit) | 588.5 | (1.0 | ) | 37.9 | 55.0 | 27.2 | 202.4 | 44.3 | 202.4 | ||||||||||||||||

| Operating (loss) income | (709.4 | ) | 66.3 | 176.5 | 210.1 | 91.9 | 216.4 | 123.6 | 216.4 | ||||||||||||||||

| Interest expense—net | (239.3 | ) | (181.9 | ) | (409.1 | ) | (413.6 | ) | (260.7 | ) | (459.5 | ) | (310.0 | ) | (315.3 | ) | |||||||||

| Loss on sale of accounts receivable | (5.9 | ) | — | (20.4 | ) | (32.4 | ) | (11.9 | ) | (10.2 | ) | (24.0 | ) | (10.2 | ) | ||||||||||

| Other income (expense) | 0.6 | (7.6 | ) | — | (2.2 | ) | 0.4 | (0.8 | ) | (1.8 | ) | (0.8 | ) | ||||||||||||

| Equity in (loss) income of unconsolidated affiliates | (86.8 | ) | (31.4 | ) | (37.5 | ) | 1.5 | (38.2 | ) | 3.0 | 0.8 | 3.0 | |||||||||||||

| Income tax benefit (expense) | 184.9 | (8.5 | ) | (30.8 | ) | (32.1 | ) | 3.8 | 25.7 | 2.4 | 25.7 | ||||||||||||||

| Minority interest in subsidiaries' loss (income) | 13.1 | (28.8 | ) | 1.5 | 6.8 | 0.5 | (1.1 | ) | 5.8 | (1.1 | ) | ||||||||||||||

| Loss from continuing operations | (842.8 | ) | (191.9 | ) | (319.8 | ) | (261.9 | ) | (214.2 | ) | (226.5 | ) | (203.2 | ) | (82.3 | ) | |||||||||

| Cumulative effect of accounting changes(b) | 0.1 | 169.7 | — | — | — | — | — | — | |||||||||||||||||

| Net loss | $ | (842.7 | ) | $ | (22.2 | ) | $ | (319.8 | ) | $ | (261.9 | ) | $ | (214.2 | ) | $ | (226.5 | ) | $ | (203.2 | ) | $ | (82.3 | ) | |

Other Data: |

|||||||||||||||||||||||||

| EBITDA(c) | $ | (590.8 | ) | $ | 320.9 | $ | 473.5 | $ | 663.5 | $ | 273.2 | $ | 617.6 | $ | 463.3 | $ | 617.6 | ||||||||

| Total unusual items of (expense) income included in EBITDA(d) | (602.0 | ) | 145.4 | (63.3 | ) | (126.2 | ) | (42.1 | ) | (220.6 | ) | (107.1 | ) | (220.6 | ) | ||||||||||

| Depreciation and amortization | 197.5 | 152.7 | 353.4 | 479.7 | 230.5 | 410.3 | 358.9 | 410.3 | |||||||||||||||||

| Capital expenditures | 76.4 | 70.2 | 191.0 | 228.9 | 129.9 | 145.0 | 167.8 | 145.0 | |||||||||||||||||

Balance Sheet Data (at period end): |

|||||||||||||||||||||||||

| Total assets | $ | 8,993.8 | $ | 8,943.1 | |||||||||||||||||||||

| Total debt | 6,200.7 | 5,128.1 | |||||||||||||||||||||||

| Total liabilities | 8,724.4 | 7,643.3 | |||||||||||||||||||||||

| Stockholders' (deficit) equity | (441.4 | ) | 1,270.6 | ||||||||||||||||||||||

13

| |

Year Ended December 31, |

Nine Months Ended September 30, |

|||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

|

|

|

Pro Forma As Adjusted |

|

|

Pro Forma As Adjusted |

||||||||||||||||||

| |

2001 |

2002 |

2003 |

2003 |

2003 |

2004 |

2003 |

2004 |

|||||||||||||||||

| |

(in millions) |

||||||||||||||||||||||||

| Net loss | $ | (842.7 | ) | $ | (22.2 | ) | $ | (319.8 | ) | $ | (261.9 | ) | $ | (214.2 | ) | $ | (226.5 | ) | $ | (203.2 | ) | $ | (82.3 | ) | |

| Depreciation and amortization | 197.5 | 152.7 | 353.4 | 479.7 | 230.5 | 410.3 | 358.9 | 410.3 | |||||||||||||||||

| Interest expense, net | 239.3 | 181.9 | 409.1 | 413.6 | 260.7 | 459.5 | 310.0 | 315.3 | |||||||||||||||||

| Income tax (benefit) expense | (184.9 | ) | 8.5 | 30.8 | 32.1 | (3.8 | ) | (25.7 | ) | (2.4 | ) | (25.7 | ) | ||||||||||||

EBITDA |

$ |

(590.8 |

) |

$ |

320.9 |

$ |

473.5 |

$ |

663.5 |

$ |

273.2 |

$ |

617.6 |

$ |

463.3 |

$ |

617.6 |

||||||||

| |

Year Ended December 31, |

Nine Months Ended September 30, |

|||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

|

|

|

Pro Forma As Adjusted |

|

|

Pro Forma As Adjusted |

||||||||||||||||||

| |

2001 |

2002 |

2003 |

2003 |

2003 |

2004 |

2003 |

2004 |

|||||||||||||||||

| |

(in millions) |

||||||||||||||||||||||||

| Early extinguishment of debt(1) | $ | (1.1 | ) | $ | (6.7 | ) | $ | — | $ | — | $ | — | $ | (1.9 | ) | $ | — | $ | (1.9 | ) | |||||

| Legal and contract settlement expense, net(2) | — | — | (2.0 | ) | (5.5 | ) | — | (6.1 | ) | (5.5 | ) | (6.1 | ) | ||||||||||||

| Loss on sale of accounts receivable(3) | (5.9 | ) | — | (20.4 | ) | (32.4 | ) | (11.9 | ) | (10.2 | ) | (24.0 | ) | (10.2 | ) | ||||||||||

| Asset write down(4) | — | — | (3.0 | ) | (5.8 | ) | (3.0 | ) | — | (5.8 | ) | — | |||||||||||||

| Restructuring, impairment and plant closing costs(5) | (588.5 | ) | 1.0 | (37.9 | ) | (55.0 | ) | (27.2 | ) | (202.4 | ) | (44.3 | ) | (202.4 | ) | ||||||||||

| Reorganization costs(6) | (6.6 | ) | (18.6 | ) | — | (27.5 | ) | — | — | (27.5 | ) | — | |||||||||||||

| Cumulative effect of accounting changes | 0.1 | 169.7 | — | — | — | — | — | — | |||||||||||||||||

Total unusual items of (expense) income included in EBITDA |

$ |

(602.0 |

) |

$ |

145.4 |

$ |

(63.3 |

) |

$ |

(126.2 |

) |

$ |

(42.1 |

) |

$ |

(220.6 |

) |

$ |

(107.1 |

) |

$ |

(220.6 |

) |

||

14

You should carefully consider the risks described below in addition to all other information provided to you in this prospectus before making an investment decision. The risks described below are not the only risks we face. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also materially and adversely affect our business operations. Any of the following risks could materially and adversely affect our business, results of operations and financial condition.

Risks Related to Our Business

We have a history of losses and may incur losses in the future, which could materially and adversely affect the market price of our common stock.

We have incurred net losses in each of the last five fiscal years and in the nine months ended September 30, 2004, and we had an accumulated deficit of $1,470 million as of September 30, 2004. We will need to generate additional revenues and/or significantly reduce costs, including interest expense, in order to avoid additional net losses in future periods. If we do achieve profitability, we may not sustain or increase profitability on a quarterly or annual basis. Failure to achieve or maintain profitability may materially and adversely affect the market price of our common stock.

Our available cash and access to additional capital may be limited by our substantial leverage, which could restrict our ability to grow our businesses.

Following this offering, we will have a substantial amount of indebtedness outstanding at our subsidiaries. As of September 30, 2004, on a pro forma as adjusted basis, we had total consolidated outstanding indebtedness of approximately $5,128.1 million (including the current portion of long-term debt). We may incur substantial additional debt from time to time for a variety of purposes. Our outstanding debt could have important consequences for our businesses, including:

The existing debt instruments of our subsidiaries contain restrictive covenants that may limit our ability to utilize our cash flow to operate our businesses by restricting our subsidiaries' ability to, among other things, make prepayments of certain debt, pay dividends to us, make investments and merge or consolidate and transfer or sell assets.

If we are unable to generate sufficient cash flow or are otherwise unable to obtain the funds required to meet payments of principal and interest on our indebtedness, or if we otherwise fail to comply with the various covenants in the instruments governing our indebtedness, we could be in default under the terms of those instruments. In the event of a default, a holder of the indebtedness could elect to declare all the funds borrowed under those instruments to be due and payable together with accrued and unpaid interest, the lenders under our credit facilities could elect to terminate their commitments thereunder and we or one or more of our subsidiaries could be forced into bankruptcy or

15

liquidation. Any of the foregoing consequences could have a material adverse effect on our business, results of operations and financial condition.

We are a holding company, with no revenue generating operations of our own. We depend on the performance of our subsidiaries and their ability to make distributions to us.

We are a holding company with no business operations, sources of income, indebtedness or assets of our own other than our ownership interests in our subsidiaries. Because all our operations are conducted by our subsidiaries, our cash flow and our ability to repay our debt that we may incur after this offering and our ability to pay dividends to our stockholders are dependent upon cash dividends and distributions or other transfers from our subsidiaries. Payment of dividends, distributions, loans or advances by our subsidiaries to us are subject to restrictions imposed by the current and future debt instruments of our subsidiaries. Moreover, our principal operating subsidiaries, HIH, HLLC and Advanced Materials, are financed separately from each other, and the debt instruments of each such subsidiary limit our ability to allocate cash flow or resources from one subsidiary, and its related group of subsidiaries, to another subsidiary group. Further, payments of dividends and other distributions by Advanced Materials may be subject to the consent of the holders of minority interests in Advanced Materials. In addition, those payments could be subject to restrictions on dividends or repatriation of earnings under applicable local law, monetary transfer restrictions and foreign currency exchange regulations in the jurisdictions in which our subsidiaries operate. As of September 30, 2004, on a pro forma as adjusted basis, our subsidiaries had total outstanding indebtedness of approximately $5,128.1 million (including the current portion of long-term debt).

Our subsidiaries are separate and distinct legal entities. Any right that we have to receive any assets of or distributions from any of our subsidiaries upon the bankruptcy, dissolution, liquidation or reorganization of any such subsidiary, or to realize proceeds from the sale of their assets, will be junior to the claims of that subsidiary's creditors, including trade creditors and holders of debt or preferred stock issued by that subsidiary.

Demand for some of our products is cyclical, and we may experience prolonged depressed market conditions for our products.

Historically, the markets for many of our products, particularly our commodity products, have experienced alternating periods of tight supply, causing prices and profit margins to increase, followed by periods of capacity additions, resulting in oversupply and declining prices and profit margins. Currently, several of our markets continue to experience conditions of oversupply, and the pricing of our products in these markets is depressed. We cannot guarantee that future growth in demand for these products will be sufficient to alleviate any existing or future conditions of excess industry capacity or that such conditions will not be sustained or further aggravated by anticipated or unanticipated capacity additions or other events.

We derive a substantial portion of our revenue from sales of commodity products. Due to the commodity nature of these products, competition in these markets is based primarily on price and to a lesser extent on performance, product quality, product deliverability and customer service. As a result, we may not be able to protect our market position for these products by product differentiation and may not be able to pass on cost increases to our customers. Historically, the prices for our commodity products have been cyclical and sensitive to relative changes in supply and demand, the availability and price of feedstocks and general economic conditions. Our other products may be subject to these same factors, but, typically, the impact of these factors is greatest on our commodity products.

16

Significant price volatility or interruptions in supply of our raw materials may result in increased costs that we may be unable to pass on to our customers, which could negatively affect our profitability.

The prices of the raw materials that we purchase from third parties are cyclical and volatile. We purchase a substantial portion of these raw materials from third party suppliers, and the cost of these raw materials represents a substantial portion of our operating expenses. The prices for a number of these raw materials generally follow price trends of, and vary with market conditions for, crude oil and natural gas feedstocks, which are highly volatile and cyclical. In recent periods, we have experienced significantly higher crude oil prices, which have resulted in increased raw material prices.

Although we frequently enter into supply agreements to acquire these raw materials, these agreements typically provide for market based pricing and provide us only limited protection against price volatility. While we attempt to match cost increases with corresponding product price increases, we are not always able to raise product prices immediately or at all. Timing differences between raw material prices, which may change daily, and contract product prices, which in many cases are negotiated only monthly or less often, have had and may continue to have a negative effect on profitability. If any of our suppliers is unable to meet its obligations under present supply agreements, we may be forced to pay higher prices to obtain the necessary raw materials from other sources and we may not be able to increase prices for our finished products to recoup the higher raw materials cost. In addition, if any of the raw materials that we use become unavailable within the geographic area from which they are now sourced, then we may not be able to obtain suitable and cost effective substitutes. Any underlying cost increase that we are not able to pass on to our customers or any interruption in supply of raw materials could have a material adverse effect on our business, results of operations and financial condition.

The industries in which we compete are highly competitive, and we may not be able to compete effectively with our competitors that have greater financial resources, which could have a material adverse effect on our business, results of operations and financial condition.

The industries in which we operate are highly competitive. Among our competitors are some of the world's largest chemical companies and major integrated petroleum companies that have their own raw material resources. Some of these companies may be able to produce products more economically than we can. In addition, some of our competitors have greater financial resources, which may enable them to invest significant capital into their businesses, including expenditures for research and development. If any of our current or future competitors develops proprietary technology that enables them to produce products at a significantly lower cost, our technology could be rendered uneconomical or obsolete. Moreover, certain of our businesses use technology that is widely available. Accordingly, barriers to entry, apart from capital availability, are low in certain product segments of our business, and the entrance of new competitors into the industry may reduce our ability to capture improving profit margins in circumstances where capacity utilization in the industry is increasing. Further, petroleum-rich countries have become more significant participants in the petrochemical industry and may expand this role significantly in the future. Increased competition in any of our businesses could compel us to reduce the prices of our products, which could result in reduced profit margins and loss of market share and have a material adverse effect on our business, results of operations and financial condition.

Our operations involve risks that may increase our operating costs, which could have a material adverse effect on our business, results of operations and financial condition.

Although we take precautions to enhance the safety of our operations and minimize the risk of disruptions, our operations are subject to hazards inherent in the manufacturing and marketing of differentiated and commodity chemical products. These hazards include: pipeline leaks and ruptures; explosions; fires; severe weather and natural disasters; mechanical failures; unscheduled downtimes;

17

labor difficulties; transportation interruptions; remediation complications; chemical spills; discharges or releases of toxic or hazardous substances or gases; storage tank leaks; and other risks. Some of these hazards can cause bodily injury and loss of life, severe damage to or destruction of property and equipment and environmental damage, and may result in suspension of operations and the imposition of civil or criminal penalties and liabilities. Furthermore, we are subject to present and future claims with respect to workplace exposure, exposure of contractors on our premises as well as other persons located nearby, workers' compensation and other matters.

We maintain property, business interruption and casualty insurance policies which we believe are in accordance with customary industry practices, but we are not fully insured against all potential hazards and risks incident to our business. As a result of market conditions, premiums and deductibles for certain insurance policies can increase substantially and, in some instances, certain insurance may become unavailable or available only for reduced amounts of coverage. If we were to incur a significant liability for which we were not fully insured, it could have a material adverse effect on our business, results of operations and financial condition.

In addition, we are subject to various claims and litigation in the ordinary course of business. We maintain insurance to cover many of our potential losses, but we are subject to various self-retentions and deductibles under our insurance. In conjunction with many of our past acquisitions, we have obtained indemnity agreements from the prior owners addressing liabilities that may arise from operations and events prior to our ownership. We are a party to several pending lawsuits and proceedings. It is possible that a judgment could be rendered against us in these cases or others in which we could be uninsured or not covered by indemnity and beyond the amounts that we currently have reserved or anticipate incurring for such matters. See "Business—Legal Proceedings."

Our independent auditors have reported several material weaknesses in our internal controls that, if not remedied, could result in material misstatements in our financial statements, cause investors to lose confidence in our reported financial information and have a negative effect on the trading price of our stock.

In connection with the audit of our financial statements for the year ended December 31, 2003, our independent auditors identified several matters that they deemed to be "material weaknesses" in our internal controls as defined in standards established by the American Institute of Certified Public Accountants. The auditors noted that these material weaknesses had led to restatements of the financial statements of certain of our subsidiaries in recent periods.

The principal material weakness identified by our auditors was that our controllership function did not have an adequate formal process in place to gather the data required to prepare the financial statements and disclosures required for the numerous financial reporting requirements of our subsidiaries. Specifically, the auditors noted that there was not a detailed review of the data supporting the disclosures in our financial statements by a senior member of our controllership function, that supporting documentation for certain disclosures was very limited, that the processes used to aggregate the information varied by subsidiary, without a standard, comprehensive package of supporting disclosure, and that information delivered to senior management and our audit committee was not timely and was often incomplete.

In addition, the auditors noted that we had made a data entry error during the transition of our PO business to the SAP enterprise resource planning system in April 2003. This error, which was not detected until February 2004, led to the restatement of the third quarter 2003 financial statements of certain of our subsidiaries, resulting in a $12.3 million increase in our net loss for the three months ended September 30, 2003. The auditors also noted that during 2003, loss on sale of accounts receivable related to our receivables securitization program was reported incorrectly due to a failure to properly understand certain aspects of the securitization program and a lack of oversight in the accounting for the program. This error led to the restatement of the financial statements of certain of

18

our subsidiaries for the first three quarters of 2003, resulting in a $17.9 million decrease in our net loss for the three months ended March 31, 2003, a $12.3 million decrease in our net loss for the three months ended June 30, 2003 and a $6.4 million decrease in our net loss for the three months ended September 30, 2003.

On October 12, 2004, we announced that we had determined to reclassify certain amounts in our consolidated statements of cash flows caused by errors in the automated process by which we determined the effect and classification of foreign exchange rates, the classification of repayment of debt by a subsidiary and the classification of certain fees paid in connection with the AdMat Transaction on our statements of cash flows. These errors led to a restatement of the financial statements of certain of our subsidiaries for the six months ended June 30, 2004 and the years ended December 31, 2003, 2002 and 2001. These reclassifications had no impact on our consolidated statements of operations or balance sheets.

We entered into a number of significant transactions in 2003, including the acquisition of the HIH minority interests and the AdMat Transaction, which significantly increased our financial reporting obligations. To improve our financial accounting organization and processes, we appointed a new independent director as the chairman of the audit committee of each of our principal subsidiaries in December 2003. In addition, since the beginning of 2004, we have replaced our Controller and have added 13 new positions in the areas of finance, treasury, internal controls and internal audit, including a Director of Financial Reporting and a Director of Internal Controls. We intend to add two more positions in internal audit before the end of the year. We have also adopted and implemented additional policies and procedures to strengthen our financial reporting system. However, the process of designing and implementing an effective financial reporting system is a continuous effort that requires us to anticipate and react to changes in our business and the economic and regulatory environments and to expend significant resources to maintain a financial reporting system that is adequate to satisfy our reporting obligations. Upon completion of this offering, we will have had only limited operating experience with the improvements we have made to date. The effectiveness of the measures we have taken to address the material weaknesses described above have not been independently tested or evaluated. We cannot assure you that the measures we have taken to date or any future measures will remediate the material weaknesses reported by our independent auditors, that we will implement and maintain adequate controls over our financial processes and reporting in the future or that we will not be required to restate our financial statements in the future. In addition, we cannot assure you that additional past or future weaknesses or significant deficiencies in our financial reporting system will not be discovered in the future.

Any failure to remediate the material weaknesses reported by our independent auditors or to implement required new or improved controls, or difficulties encountered in their implementation, could cause us to fail to meet our reporting obligations or result in material misstatements in our financial statements. Any such failure also could adversely affect the results of the periodic management evaluations and annual auditor attestation reports regarding the effectiveness of our "internal control over financial reporting" that will be required when the SEC's rules under Section 404 of the Sarbanes-Oxley Act of 2002 become applicable to us beginning with our Annual Report on Form 10-K for the year ending December 31, 2005 to be filed in early 2006. Inferior internal controls could also cause investors to lose confidence in our reported financial information, which could have a negative effect on the trading price of our stock.

We are subject to many environmental and safety regulations that may result in unanticipated costs or liabilities, which could have a material adverse effect on our business, results of operations and financial condition.

We are subject to extensive federal, state, local and foreign laws, regulations, rules and ordinances relating to pollution, protection of the environment and the generation, storage, handling,

19

transportation, treatment, disposal and remediation of hazardous substances and waste materials. Actual or alleged violations of environmental laws or permit requirements could result in restrictions or prohibitions on plant operations, substantial civil or criminal sanctions, as well as, under some environmental laws, the assessment of strict liability and/or joint and several liability. Moreover, changes in environmental regulations could inhibit or interrupt our operations, or require us to modify our facilities or operations. Accordingly, environmental or regulatory matters may cause us to incur significant unanticipated losses, costs or liabilities, which could have a material adverse effect on our business, results of operations and financial condition. See "Business—Environmental, Health and Safety Matters."

In addition, we could incur significant expenditures in order to comply with existing or future environmental or safety laws. Capital expenditures and costs relating to environmental or safety matters will be subject to evolving regulatory requirements and will depend on the timing of the promulgation and enforcement of specific standards which impose requirements on our operations. Therefore, we cannot assure you that capital expenditures and costs beyond those currently anticipated will not be required under existing or future environmental or safety laws.

Furthermore, we may be liable for the costs of investigating and cleaning up environmental contamination on or from our properties or at off-site locations where we disposed of or arranged for the disposal or treatment of hazardous materials or from disposal activities that pre-dated the purchase of our businesses. We cannot assure you that additional costs and expenditures beyond those currently anticipated will not be incurred to address all such known and unknown situations under existing and future environmental law. See "Business—Environmental, Health and Safety Matters."

Existing or future litigation or legislative initiatives restricting the use of MTBE in gasoline may subject us or our products to environmental liability or materially adversely affect our sales and costs.

We produce MTBE, an oxygenate that is blended with gasoline to reduce vehicle air emissions and to enhance the octane rating of gasoline. The use of MTBE is controversial in the U.S. and elsewhere and may be substantially curtailed or eliminated in the future by legislation or regulatory action. For example, California, New York and Connecticut have adopted rules that prohibit the use of MTBE in gasoline sold in those states as of January 1, 2004. Overall, states that have taken some action to prohibit or restrict the use of MTBE in gasoline account for a substantial portion of the "pre-ban" U.S. MTBE market. Additional phase-outs or other future regulation of MTBE may result in a significant reduction in demand for our MTBE, a material loss in revenues or material increase in compliance costs or expenditures. In addition, a number of lawsuits have been filed, primarily against gasoline manufacturers, marketers and distributors, by persons seeking to recover damages allegedly arising from the presence of MTBE in groundwater. While we have not been named as a defendant in any litigation concerning the environmental effects of MTBE, we cannot provide assurances that we will not be involved in any such litigation or that such litigation will not have a material adverse effect on our business, results of operations and financial condition. See "Business—Environmental, Health and Safety Matters."

Our results of operations may be adversely affected by fluctuations in currency exchange rates and international business risks.

Some of our subsidiaries conduct a significant portion of their business outside the U.S. These operations outside the U.S. are subject to risks normally associated with international operations. These risks include the need to convert currencies which may be received for our products into currencies in which our subsidiaries purchase raw materials or pay for services, which could result in a gain or loss depending on fluctuations in exchange rates. In addition, we translate our local currency financial results into U.S. dollars based on average exchange rates prevailing during the reporting period or the exchange rate at the end of that period. During times of a strengthening U.S. dollar, our reported

20

international sales and earnings may be reduced because the local currency may translate into fewer U.S. dollars.

Other risks of international operations include trade barriers, tariffs, exchange controls, national and regional labor strikes, social and political risks, general economic risks and required compliance with a variety of foreign laws, including tax laws and the difficulty of enforcing agreements and collecting receivables through foreign legal systems. The occurrence of these risks could adversely affect the businesses of our international subsidiaries, which could significantly affect their ability to make distributions to us.

Our business is dependent on our intellectual property. If our patents are declared invalid or our trade secrets become known to our competitors, our ability to compete may be adversely affected.

Proprietary protection of our processes, apparatuses and other technology is important to our business. Consequently, we may have to rely on judicial enforcement of our patents and other proprietary rights. While a presumption of validity exists with respect to patents issued to us in the U.S., there can be no assurance that any of our patents will not be challenged, invalidated, circumvented or rendered unenforceable. Furthermore, if any pending patent application filed by us does not result in an issued patent, or if patents are issued to us, but such patents do not provide meaningful protection of our intellectual property, then our ability to compete may be adversely affected. Additionally, our competitors or other third parties may obtain patents that restrict or preclude our ability to lawfully produce or sell our products in a competitive manner, which could have a material adverse effect on our business, results of operations and financial condition.

We also rely upon unpatented proprietary know-how and continuing technological innovation and other trade secrets to develop and maintain our competitive position. While it is our policy to enter into confidentiality agreements with our employees and third parties to protect our intellectual property, these confidentiality agreements may be breached, may not provide meaningful protection for our trade secrets or proprietary know-how, or adequate remedies may not be available in the event of an unauthorized use or disclosure of such trade secrets and know-how. In addition, others could obtain knowledge of such trade secrets through independent development or other access by legal means. The failure of our patents or confidentiality agreements to protect our processes, apparatuses, technology, trade secrets or proprietary know-how could have a material adverse effect on our business, results of operations and financial condition.

Loss of key members of our management could adversely affect our business.

We depend on the continued employment and performance of our senior executives and other key members of management. If any of these individuals resigns or becomes unable to continue in his present role and is not adequately replaced, our business operations could be materially adversely affected. We generally do not have employment agreements with, and we do not maintain any "key man" life insurance for, any of our executive officers. See "Management."

Terrorist attacks, such as the attacks that occurred on September 11, 2001, the continuing military action in Iraq, general instability in various OPEC member nations, the threat of other attacks or acts of war in the U.S. and abroad and increased security regulations related to our industry could adversely affect our business.

The attacks of September 11, 2001, and subsequent events, including the continuing military action in Iraq, have caused instability in the U.S. and other financial markets and have led, and may continue to lead, to further armed hostilities, prolonged military action in Iraq, or further acts of terrorism in the U.S. or abroad, which could cause further instability in financial markets. Current regional tensions and conflicts in various OPEC member nations, including the continuing military action in Iraq, have caused, and may cause further, increases in raw material costs, particularly crude oil and natural gas

21

feedstocks, which are used in our operations. The uncertainty surrounding the continuing military action in Iraq and the threat of further armed hostilities or acts of terrorism may impact any or all of our physical facilities and operations, which are located in North America, Europe, Australia, Asia, Africa, South America and the Middle East, or those of our customers. Furthermore, the terrorist attacks, subsequent events and future developments in any of these areas may result in reduced demand from our customers for our products. In addition, local, state and federal governments have begun a regulatory process that could lead to new regulations impacting the security of chemical plant locations and the transportation of hazardous chemicals, which could result in higher operating costs. These developments will subject our worldwide operations to increased risks and, depending on their magnitude, could have a material adverse effect on our business, results of operations and financial condition.

Future acquisitions, partnerships and joint ventures may require significant resources and/or result in unanticipated adverse consequences that could adversely affect our business, results of operations and financial condition.