UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934 (Amendment No. )

| Filed by the Registrant x | |||

| Filed by a Party other than the Registrant ¨ | |||

| Check the appropriate box: | |||

| ¨ | Preliminary Proxy Statement | ||

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | ||

| ¨ | Definitive Proxy Statement | ||

| x | Definitive Additional Materials | ||

| ¨ | Soliciting Material under §240.14a-12 | ||

|

Huntsman Corporation | |||

|

(Name of Registrant as Specified In Its Charter) | |||

| (Name of Person(s) Filing Proxy Statement, if other than the Registrant) | |||

| Payment of Filing Fee (Check all boxes that apply): | |||

| x | No fee required | ||

| ¨ | Fee paid previously with preliminary materials | ||

| ¨ | Fee computed on table in exhibit required by Item 25(b) per Exchange Act Rules 14a-6(i)(1) and 0-11 | ||

| |

|

| FOR IMMEDIATE RELEASE | Media: | Investor Relations: |

| March 16, 2022 | Gary Chapman | Ivan Marcuse |

| The Woodlands, TX | (281) 719-4324 | (281) 719-4637 |

| NYSE: HUN |

Huntsman Chairman and CEO Issues Open Letter to Shareholders

Emphasizes successful execution of strategic plan, historic results and 5-Year TSR of 91%1, substantial progress achieving 2022-2024 targets

Highlights fully refreshed and fit for purpose Board holding management accountable

Urges Shareholders to Vote “FOR ALL” of Huntsman’s Highly Qualified Director Nominees on the WHITE Proxy Card

THE WOODLANDS, TX – Peter R. Huntsman, Chairman of the Board of Directors of Huntsman Corporation (NYSE: HUN), issued the following letter to all Huntsman’s shareholders in advance of its upcoming 2022 Annual Meeting of Stockholders, scheduled to be held on March 25, 2022:

Dear Fellow Shareholders,

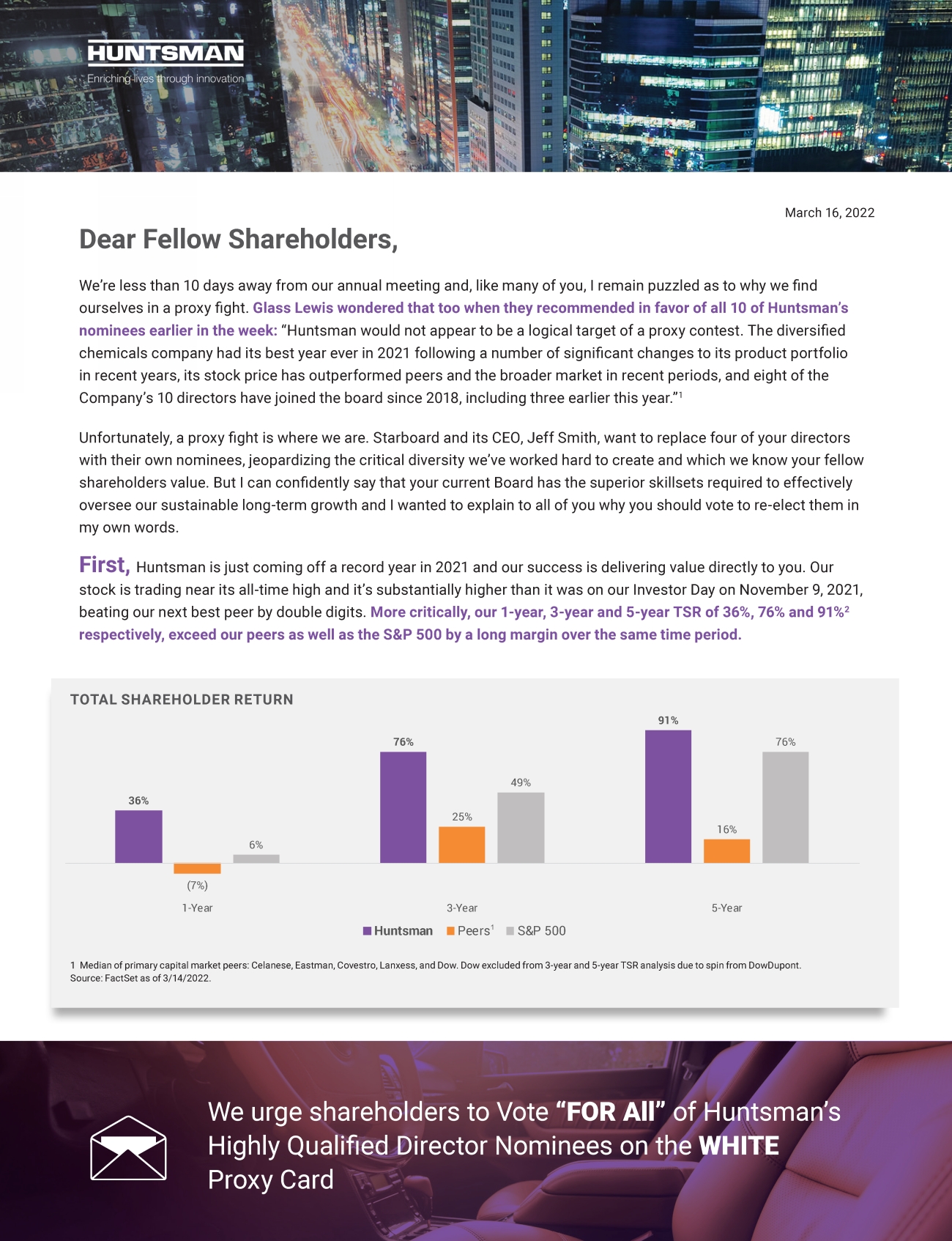

We’re less than 10 days away from our annual meeting and, like many of you, I remain puzzled as to why we find ourselves in a proxy fight. Glass Lewis wondered about that too when they recommended in favor of all 10 of Huntsman’s nominees earlier in the week: “Huntsman would not appear to be a logical target of a proxy contest. The diversified chemicals company had its best year ever in 2021 following a number of significant changes to its product portfolio in recent years, its stock price has outperformed peers and the broader market in recent periods, and eight of the Company’s 10 directors have joined the board since 2018, including three earlier this year.”2

Unfortunately, a proxy fight is where we are. Starboard and its CEO, Jeff Smith, want to replace four of your directors with their own nominees, jeopardizing the critical diversity we’ve worked hard to create and which we know your fellow shareholders value. But I can confidently say that your current Board has the superior skillsets required to effectively oversee our sustainable long-term growth and I wanted to explain to all of you why you should vote to re-elect them in my own words.

1 Timeframe of March 14, 2017 through March 14, 2022.

2 Glass Lewis Report, March 13, 2022. Permission to use quotations from Glass Lewis Report neither sought nor obtained.

- 1 -

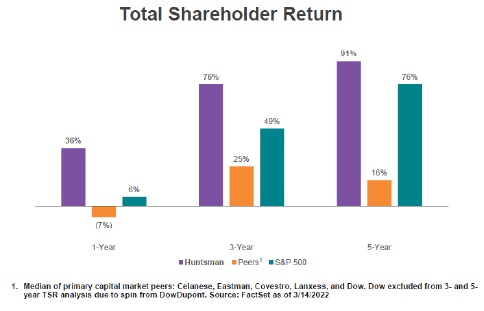

First, Huntsman is just coming off a record year in 2021 and our success is delivering value directly to you. Our stock is trading near its all-time high and it’s substantially higher than it was on our Investor Day on November 9, 2021, beating our next best peer by double digits. More critically, our 1-year, 3-year and 5-year TSR of 36%, 76% and 91%3 respectively, exceed our peers as well as the S&P 500 by a long margin over the same time period.

I don’t believe we need to replace any members of a Board that is already fully refreshed and fit for purpose under these circumstances and doing so puts the value we’ve created for you at risk and threatens to kill the momentum we’ve been developing.

Over the past few years, the Board has taken meaningful actions to oversee our ‘value over volume’ strategy, transform our balance sheet, and enhance our governance through an extensive refreshment plan. As a result of all these actions, 2021 was the very best year in our history with the strongest profit and margin performance we’ve ever achieved with our current portfolio. I’m incredibly proud that we’ve successfully transformed Huntsman into a downstream and differentiated chemical business and I am confident that we’re perfectly positioned – especially under the oversight of our fully refreshed Board with its well-constructed mix of expertise, experience, perspective and diversity – to take the Company forward.

3 Timeframes measured from respective starting dates of March 14, 2021; March 14, 2019 and March 14, 2017 through March 14, 2022.

- 2 -

Second, Starboard has been criticizing us for failing to meet the performance targets we set in 2014, 2016 and 2018 and we’ve tried to explain why those criticisms were not well founded. Here, I want to focus you on our future. I want to remind you of our 2021 Investor Day targets and tell you how far along the path to meeting them we’ve already come.

The record results we delivered in 2021 were used as the baseline for a robust set of specific operational and financial goals we announced at our November 2021 Investor Day. Those goals focus on key financial metrics that long-term shareholders care most about – Adjusted EBITDA margin, cost optimization, and free cash flow – and the results coming out of our four divisions on each of these metrics to date are excellent.

As you know, after reporting a record third quarter last October, we reported a record fourth quarter and record full year 2021 earnings on February 15, noting that our adjusted EBITDA for Q4 was $349 million, a 45% increase from prior year, that free cash flow from continuing operations was just under $700 million, and that we had demonstrated sustainable growth and margin improvement. We also provided positive guidance for Q1 2022 but just three weeks later, on March 7, we had to increase that guidance and reported that we were now expecting adjusted EBITDA in the first quarter “would be at or even above the high end of the previously communicated range of $350 million to $380 million, and that adjusted EBITDA margin for the first quarter was trending to 17% even in the face of significant energy cost escalation in Europe.”

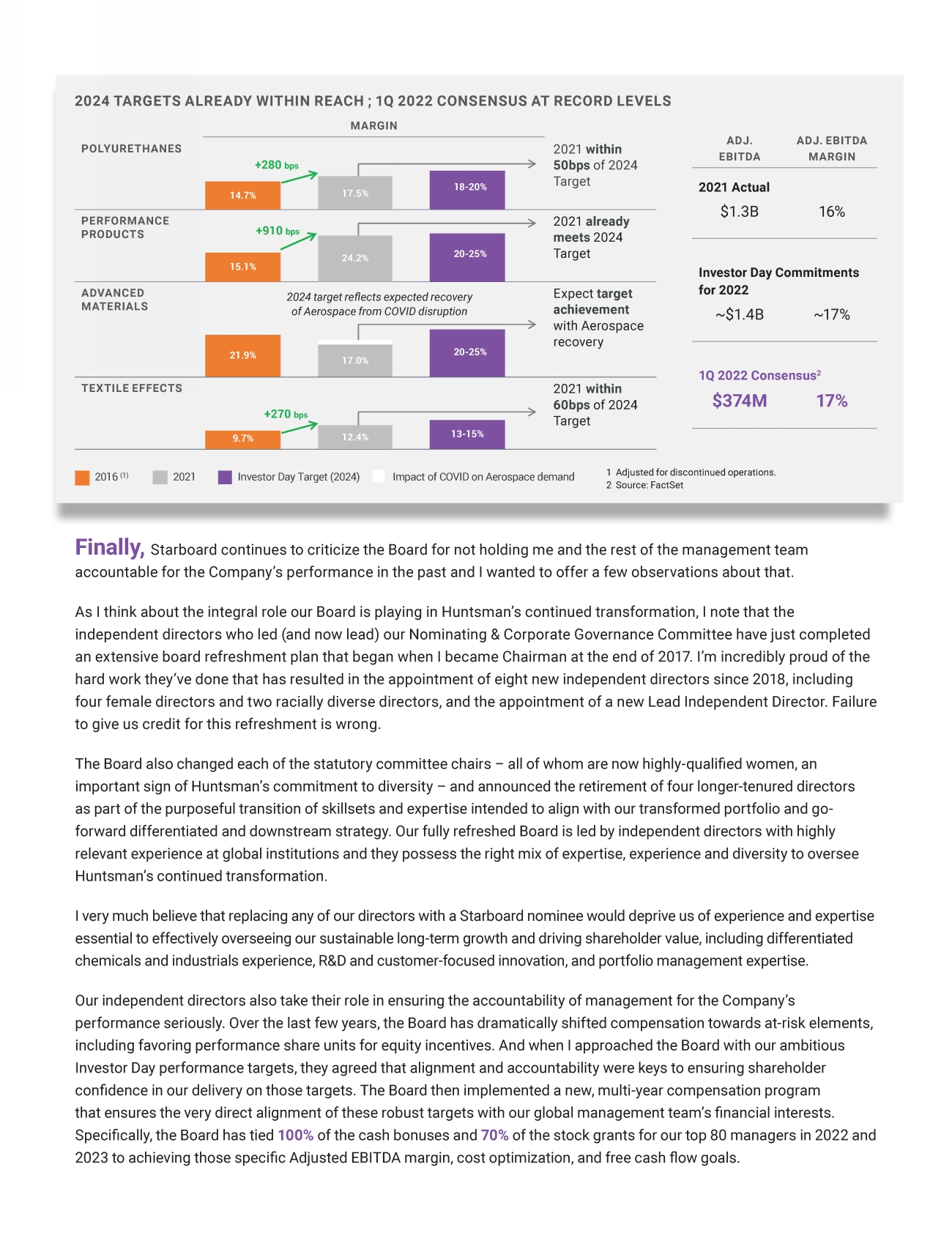

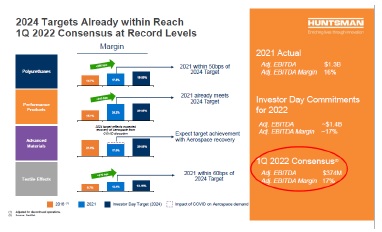

Moreover, by the end of 2021, each of our four divisions was already well on their way to meeting the adjusted EBITDA margin targets we said they would reach by 2024 (one has already met its 2024 target) and each division had also identified specific improvements to ensure those target were timely met. Half of the $240 million in identified cost savings and synergies has been delivered ahead of schedule and we have clear line of sight to a total of 300-350 basis points of improvement, including execution of in progress investments aligned with upgrading our polyurethanes portfolio, as well as targeted projects into the electric vehicle, energy-saving insulation and semiconductor markets. The quantifiable progress we’ve made to date, shown below, demonstrates that we are on the right path to delivering you the value we promised.

- 3 -

Finally, Starboard continues to criticize the Board for not holding me and the rest of the management team accountable for the Company’s performance in the past and I wanted to offer a few observations about that.

As I think about the integral role our Board is playing in Huntsman’s continued transformation, I note that the independent directors who led (and now lead) our Nominating & Corporate Governance Committee have just completed an extensive board refreshment plan that began when I became Chairman at the end of 2017. I’m incredibly proud of the hard work they’ve done that has resulted in the appointment of eight new independent directors since 2018, including four female directors and two racially diverse directors, and the appointment of a new Lead Independent Director. Failure to give us credit for this refreshment is wrong.

The Board also changed each of the statutory committee chairs – all of whom are now highly-qualified women, an important sign of Huntsman’s commitment to diversity – and announced the retirement of four longer-tenured directors as part of the purposeful transition of skillsets and expertise intended to align with our transformed portfolio and go-forward differentiated and downstream strategy. Our fully refreshed Board is led by independent directors with highly relevant experience at global institutions and they possess the right mix of expertise, experience and diversity to oversee Huntsman’s continued transformation.

I very much believe that replacing any of our directors with a Starboard nominee would deprive us of experience and expertise essential to effectively overseeing our sustainable long-term growth and driving shareholder value, including differentiated chemicals and industrials experience, R&D and customer-focused innovation, and portfolio management expertise.

Our independent directors also take their role in ensuring the accountability of management for the Company’s performance seriously. Over the last few years, the Board has dramatically shifted compensation towards at-risk elements, including favoring performance share units for equity incentives. And when I approached the Board with our ambitious Investor Day performance targets, they agreed that alignment and accountability were keys to ensuring shareholder confidence in our delivery on those targets. The Board then implemented a new, multi-year compensation program that ensures the very direct alignment of these robust targets with our global management team’s financial interests. Specifically, the Board has tied 100% of the cash bonuses and 70% of the stock grants for our top 80 managers in 2022 and 2023 to achieving those specific Adjusted EBITDA margin, cost optimization, and free cash flow goals.

- 4 -

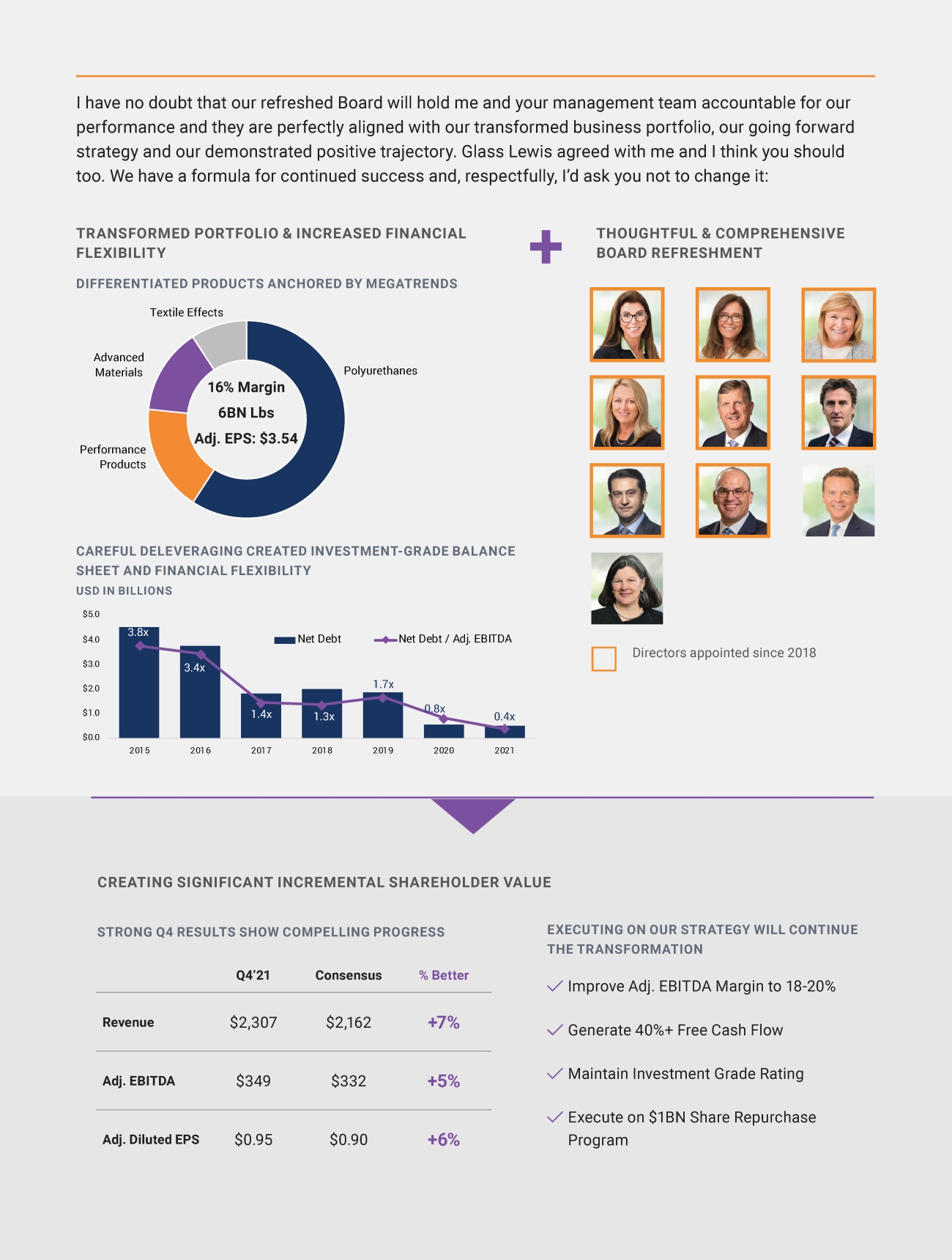

I have no doubt that our refreshed Board will hold me and your management team accountable for our performance and they are perfectly aligned with our transformed business portfolio, our going forward strategy and our demonstrated positive trajectory. Glass Lewis agreed with me and I think you should too. We have a formula for continued success and, respectfully, I’d ask you not to change it:

Nor is there any doubt that your Board is delivering real value to you right now and it is primed to continue delivering value as they oversee the Company’s execution. As Glass Lewis concluded in its recent report, there is just no reason to change course:

Huntsman’s recent financial and stock price performance indicate the Company is on the right track and, ultimately, we fail to see a compelling case that further changes beyond those the board has already made are either warranted at this time or likely to result in incremental improvement. Further, the Dissident’s campaign appears to be backwards-looking in several respects, in our view, and we believe it lacks new ideas or a detailed plan to improve Huntsman’s performance going forward. Considering there is little if any disagreement between the Company and the Dissident on Huntsman’s strategy and objectives – only execution and accountability – the matter seems to boil down to which nominees are better qualified and situated to oversee the Company’s management and direction. Although Starboard seeks to replace directors who it believes lack true independence or qualifications for the board, not only do we find insufficient cause to remove current directors, we also aren’t convinced that Starboard’s nominees have particularly relevant, timely or incremental experience to add to the board at this time.4

4 Glass Lewis Report, March 13, 2022. Permission to use quotations from Glass Lewis Report neither sought nor obtained.

- 5 -

Thank you for taking some time to read this note. I would have preferred to have spoken with each and every one of you face to face, but that just wasn’t possible with only a week or so before your votes have to be in. On that point, I would like to remind you that every vote is important no matter how many shares it represents, and I would also urge you to discard any blue proxy materials you may have received and only vote using the WHITE proxy card.

If you need help voting your shares, you can call toll-free our proxy solicitor, Innisfree M&A Incorporated, at (877) 750-0926, and you can find additional relevant material regarding the Board’s voting recommendations for the 2022 Annual Meeting online at voteforhuntsman.com.

Thank you again,

Peter R. Huntsman

Advisors:

BofA Securities and Moelis & Company LLC are serving as financial advisors to Huntsman. Kirkland & Ellis LLP is serving as legal advisor to Huntsman.

About Huntsman:

Huntsman Corporation is a publicly traded global manufacturer and marketer of differentiated and specialty chemicals with 2021 revenues of approximately $8 billion. Our chemical products number in the thousands and are sold worldwide to manufacturers serving a broad and diverse range of consumer and industrial end markets. We operate more than 70 manufacturing, R&D and operations facilities in approximately 30 countries and employ approximately 9,000 associates within our four distinct business divisions. For more information about Huntsman, please visit the company’s website at www.huntsman.com.

Social Media:

Twitter: www.twitter.com/Huntsman_Corp

Facebook: www.facebook.com/huntsmancorp

LinkedIn: www.linkedin.com/company/huntsman

- 6 -

Forward-Looking Statements:

This release includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements include statements concerning our plans, objectives, goals, financial targets, strategies, future events, future revenue or performance, capital expenditures, plans or intentions relating to acquisitions, divestitures or strategic transactions, including the review of the Textile Effects Division, business trends and any other information that is not historical information. When used in this release, the words “estimates,” “expects,” “anticipates,” “likely,” “projects,” “outlook,” “plans,” “intends,” “believes,” “forecasts,” “targets,” or future or conditional verbs, such as “will,” “should,” “could” or “may,” and variations of such words or similar expressions are intended to identify forward-looking statements. These forward-looking statements, including, without limitation, management’s examination of historical operating trends and data, are based upon our current expectations and various assumptions and beliefs. In particular, such forward-looking statements are subject to uncertainty and changes in circumstances and involve risks and uncertainties that may affect the Company’s operations, markets, products, prices and other factors as discussed in the Company’s filings with the Securities and Exchange Commission (the “SEC”). In addition, there can be no assurance that the review of the Textile Effects Division will result in one or more transactions or other strategic change or outcome. Significant risks and uncertainties may relate to, but are not limited to, ongoing impact of COVID-19 on our operations and financial results, volatile global economic conditions, cyclical and volatile product markets, disruptions in production at manufacturing facilities, timing of proposed transactions, reorganization or restructuring of the Company’s operations, including any delay of, or other negative developments affecting the ability to implement cost reductions and manufacturing optimization improvements in the Company’s businesses and to realize anticipated cost savings, and other financial, operational, economic, competitive, environmental, political, legal, regulatory and technological factors. Any forward-looking statement should be considered in light of the risks set forth under the caption “Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2021, which may be supplemented by other risks and uncertainties disclosed in any subsequent reports filed or furnished by the Company from time to time. All forward-looking statements apply only as of the date made. Except as required by law, the Company undertakes no obligation to update or revise forward-looking statements to reflect events or circumstances that arise after the date made or to reflect the occurrence of unanticipated events.

Non-GAAP Financial Measures:

This release contains financial measures that are not in accordance with generally accepted accounting principles in the U.S. (“GAAP”), including adjusted EBITDA and free cash flow. For more information on the non-GAAP financial measures used by the Company and referenced in this press release, including definitions and reconciliations of non-GAAP measures to GAAP, please refer to the “Non-GAAP Reconciliation” hyperlink available in the “Financials” section of the Company’s website at www.huntsman.com/investors.

The Company does not provide reconciliations of forward-looking non-GAAP financial measures to the most comparable GAAP financial measures on a forward-looking basis because the Company is unable to provide a meaningful or accurate calculation or estimation of reconciling items and the information is not available without unreasonable effort. This is due to the inherent difficulty of forecasting the timing and amount of certain items, such as, but not limited to, (a) business acquisition and integration expenses, (b) merger costs, and (c) certain legal and other settlements and related costs. Each of such adjustments has not yet occurred, are out of the Company’s control and/or cannot be reasonably predicted. For the same reasons, the Company is unable to address the probable significance of the unavailable information.

Contacts:

Investors

Ivan Marcuse

VP, Investor Relations

Huntsman Corporation

(281) 719-4637

Or

Scott Winter / Jonathan Salzberger

Innisfree M&A Incorporated

(212) 750-5833

Media

Gary Chapman

Huntsman Corporation

(281) 719-4324

Or

Steve Frankel / Meaghan Repko / Amy Feng

Joele Frank, Wilkinson Brimmer Katcher

(212) 355-4449

- 7 -

| March 16, 2022 Dear Fellow Shareholders, We’re less than 10 days away from our annual meeting and, like many of you, I remain puzzled as to why we find ourselves in a proxy fight. Glass Lewis wondered that too when they recommended in favor of all 10 of Huntsman’s nominees earlier in the week: “Huntsman would not appear to be a logical target of a proxy contest. The diversified chemicals company had its best year ever in 2021 following a number of significant changes to its product portfolio in recent years, its stock price has outperformed peers and the broader market in recent periods, and eight of the Company’s 10 directors have joined the board since 2018, including three earlier this year.”1 Unfortunately, a proxy fight is where we are. Starboard and its CEO, Jeff Smith, want to replace four of your directors with their own nominees, jeopardizing the critical diversity we’ve worked hard to create and which we know your fellow shareholders value. But I can confidently say that your current Board has the superior skillsets required to effectively oversee our sustainable long-term growth and I wanted to explain to all of you why you should vote to re-elect them in my own words. First, Huntsman is just coming off a record year in 2021 and our success is delivering value directly to you. Our stock is trading near its all-time high and it’s substantially higher than it was on our Investor Day on November 9, 2021, beating our next best peer by double digits. More critically, our 1-year, 3-year and 5-year TSR of 36%, 76% and 91%2 respectively, exceed our peers as well as the S&P 500 by a long margin over the same time period. 1 Median of primary capital market peers: Celanese, Eastman, Covestro, Lanxess, and Dow. Dow excluded from 3-year and 5-year TSR analysis due to spin from DowDupont. Source: FactSet as of 3/14/2022. TOTAL SHAREHOLDER RETURN We urge shareholders to Vote “FOR All” of Huntsman’s Highly Qualified Director Nominees on the WHITE Proxy Card 36% 76% 91% (7%) 25% 16% 6% 49% 76% 1-Year 3-Year 5-Year Huntsman Peers S&P 500 1 |

| I don’t believe we need to replace any members of a Board that is already fully refreshed and fit for purpose under these circumstances and doing so puts the value we’ve created for you at risk and threatens to kill the momentum we’ve been developing. Over the past few years, the Board has taken meaningful actions to oversee our ‘value over volume’ strategy, transform our balance sheet, and enhance our governance through an extensive refreshment plan. As a result of all these actions, 2021 was the very best year in our history with the strongest profit and margin performance we’ve ever achieved with our current portfolio. I’m incredibly proud that we’ve successfully transformed Huntsman into a downstream and differentiated chemical business and I am confident that we’re perfectly positioned — especially under the oversight of our fully refreshed Board with its well-constructed mix of expertise, experience, perspective and diversity — to take the Company forward. Second, Starboard has been criticizing us for failing to meet the performance targets we set in 2014, 2016 and 2018 and we’ve tried to explain why those criticisms were not well founded. Here, I want to focus you on our future. I want to remind you of our 2021 Investor Day targets and tell you how far along the path to meeting them we’ve already come. The record results we delivered in 2021 were used as the baseline for a robust set of specific operational and financial goals we announced at our November 2021 Investor Day. Those goals focus on key financial metrics that long-term shareholders care most about — Adjusted EBITDA margin, cost optimization, and free cash flow — and the results coming out of our four divisions on each of these metrics to date are excellent. As you know, after reporting a record third quarter last October, we reported a record fourth quarter and record full year 2021 earnings on February 15, noting that our adjusted EBITDA for Q4 was $349 million, a 45% increase from prior year, that free cash flow from continuing operations was just under $700 million, and that we had demonstrated sustainable growth and margin improvement. We also provided positive guidance for Q1 2022 but just three weeks later, on March 7, we had to increase that guidance and reported that we were now expecting adjusted EBITDA in the first quarter “would be at or even above the high end of the previously communicated range of $350 million to $380 million, and that adjusted EBITDA margin for the first quarter was trending to 17% even in the face of significant energy cost escalation in Europe.” Moreover, by the end of 2021, each of our four divisions was already well on their way to meeting the adjusted EBITDA margin targets we said they would reach by 2024 (one has already met its 2024 target) and each division had also identified specific improvements to ensure those target were timely met. Half of the $240 million in identified cost savings and synergies has been delivered ahead of schedule and we have clear line of sight to a total of 300-350 basis points of improvement, including execution of in progress investments aligned with upgrading our polyurethanes portfolio, as well as targeted projects into the electric vehicle, energy-saving insulation and semiconductor markets. The quantifiable progress we’ve made to date, shown below, demonstrates that we are on the right path to delivering you the value we promised. Reject Starboard and vote “FOR ALL” of Huntsman’s nominees on the WHITE proxy card. |

| Finally, Starboard continues to criticize the Board for not holding me and the rest of the management team accountable for the Company’s performance in the past and I wanted to offer a few observations about that. As I think about the integral role our Board is playing in Huntsman’s continued transformation, I note that the independent directors who led (and now lead) our Nominating & Corporate Governance Committee have just completed an extensive board refreshment plan that began when I became Chairman at the end of 2017. I’m incredibly proud of the hard work they’ve done that has resulted in the appointment of eight new independent directors since 2018, including four female directors and two racially diverse directors, and the appointment of a new Lead Independent Director. Failure to give us credit for this refreshment is wrong. The Board also changed each of the statutory committee chairs – all of whom are now highly-qualified women, an important sign of Huntsman’s commitment to diversity – and announced the retirement of four longer-tenured directors as part of the purposeful transition of skillsets and expertise intended to align with our transformed portfolio and go- forward differentiated and downstream strategy. Our fully refreshed Board is led by independent directors with highly relevant experience at global institutions and they possess the right mix of expertise, experience and diversity to oversee Huntsman’s continued transformation. I very much believe that replacing any of our directors with a Starboard nominee would deprive us of experience and expertise essential to effectively overseeing our sustainable long-term growth and driving shareholder value, including differentiated chemicals and industrials experience, R&D and customer-focused innovation, and portfolio management expertise. Our independent directors also take their role in ensuring the accountability of management for the Company’s performance seriously. Over the last few years, the Board has dramatically shifted compensation towards at-risk elements, including favoring performance share units for equity incentives. And when I approached the Board with our ambitious Investor Day performance targets, they agreed that alignment and accountability were keys to ensuring shareholder confidence in our delivery on those targets. The Board then implemented a new, multi-year compensation program that ensures the very direct alignment of these robust targets with our global management team’s financial interests. Specifically, the Board has tied 100% of the cash bonuses and 70% of the stock grants for our top 80 managers in 2022 and 2023 to achieving those specific Adjusted EBITDA margin, cost optimization, and free cash flow goals. 1 Adjusted for discontinued operations. 2 Source: FactSet 2024 TARGETS ALREADY WITHIN REACH ; 1Q 2022 CONSENSUS AT RECORD LEVELS MARGIN POLYURETHANES 2021 within 50bps of 2024 Target PERFORMANCE PRODUCTS 2021 already meets 2024 Target ADVANCED MATERIALS Expect target achievement with Aerospace recovery TEXTILE EFFECTS 2021 within 60bps of 2024 Target ADJ. EBITDA ADJ. EBITDA MARGIN 2021 Actual $1.3B 16% Investor Day Commitments for 2022 ~$1.4B ~17% 1Q 2022 Consensus2 $374M 17% 14.7% 17.5% 18-20% +280 bps 15.1% 24.2% 20-25% +910 bps 17.0% 21.9% 20-25% 9.7% 12.4% 13-15% +270 bps 2016 (1) 2021 Investor Day Target (2024) Impact of COVID on Aerospace demand 2024 target reflects expected recovery of Aerospace from COVID disruption |

| I have no doubt that our refreshed Board will hold me and your management team accountable for our performance and they are perfectly aligned with our transformed business portfolio, our going forward strategy and our demonstrated positive trajectory. Glass Lewis agreed with me and I think you should too. We have a formula for continued success and, respectfully, I’d ask you not to change it: THOUGHTFUL & COMPREHENSIVE BOARD REFRESHMENT TRANSFORMED PORTFOLIO & INCREASED FINANCIAL FLEXIBILITY Directors appointed since 2018 CREATING SIGNIFICANT INCREMENTAL SHAREHOLDER VALUE + EXECUTING ON OUR STRATEGY WILL CONTINUE THE TRANSFORMATION Improve Adj. EBITDA Margin to 18-20% Generate 40%+ Free Cash Flow Maintain Investment Grade Rating Execute on $1BN Share Repurchase Program STRONG Q4 RESULTS SHOW COMPELLING PROGRESS Q4’21 Consensus % Better Revenue $2,307 $2,162 +7% Adj. EBITDA $349 $332 +5% Adj. Diluted EPS $0.95 $0.90 +6% CAREFUL DELEVERAGING CREATED INVESTMENT-GRADE BALANCE SHEET AND FINANCIAL FLEXIBILITY USD IN BILLIONS DIFFERENTIATED PRODUCTS ANCHORED BY MEGATRENDS Polyurethanes Performance Products Advanced Materials Textile Effects 16% Margin 6BN Lbs Adj. EPS: $3.54 3.8x 3.4x 1.4x 1.3x 1.7x 0.8x 0.4x 0 . 0x 1 . 0x 2 . 0x 3 . 0x 4 . 0x 5 . 0x $0.0 $1.0 $2.0 $3.0 $4.0 $5.0 2015 2016 2017 2018 2019 2020 2021 Net Debt Net Debt / Adj. EBITDA |

| Nor is there any doubt that your Board is delivering real value to you right now and it is primed to continue delivering value as they oversee the Company’s execution. As Glass Lewis concluded in its recent report, there is just no reason to change course: Huntsman’s recent financial and stock price performance indicate the Company is on the right track and, ultimately, we fail to see a compelling case that further changes beyond those the board has already made are either warranted at this time or likely to result in incremental improvement. Further, the Dissident’s campaign appears to be backwards-looking in several respects, in our view, and we believe it lacks new ideas or a detailed plan to improve Huntsman’s performance going forward. Considering there is little if any disagreement between the Company and the Dissident on Huntsman’s strategy and objectives – only execution and accountability – the matter seems to boil down to which nominees are better qualified and situated to oversee the Company’s management and direction. Although Starboard seeks to replace directors who it believes lack true independence or qualifications for the board, not only do we find insufficient cause to remove current directors, we also aren’t convinced that Starboard’s nominees have particularly relevant, timely or incremental experience to add to the board at this time.3 Thank you for taking some time to read this note. I would have preferred to have spoken with each and every one of you face to face, but that just wasn’t possible with only a week or so before your votes have to be in. On that point, I would like to remind you that every vote is important no matter how many shares it represents, and I would also urge you to discard any blue proxy materials you may have received and only vote using the WHITE proxy card. If you need help voting your shares, you can call toll-free our proxy solicitor, Innisfree M&A Incorporated, at (877) 750-0926, and you can find additional relevant material regarding the Board’s voting recommendations for the 2022 Annual Meeting online at voteforhuntsman.com. Thank you again, PETER R. HUNTSMAN Vote “FOR ALL” of Huntsman’s nominees on the WHITE PROXY CARD. |

| 1 Glass Lewis Report, March 13, 2022. Permission to use quotations from Glass Lewis Report neither sought nor obtained. 2 Timeframes measured from respective starting dates of March 14, 2021; March 14, 2019 and March 14, 2017 through March 14, 2022. 3 Glass Lewis Report, March 13, 2022. Permission to use quotations from Glass Lewis Report neither sought nor obtained. Forward-Looking Statements: This communication includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements include statements concerning our plans, objectives, goals, financial targets, strategies, future events, future revenue or performance, capital expenditures, financing needs, plans or intentions relating to acquisitions, divestitures or strategic transactions, including the review of the Textile Effects Division, business trends and any other information that is not historical information. When used in this communication, the words “estimates,” “expects,” “anticipates,” “likely,” “projects,” “outlook,” “plans,” “intends,” “believes,” “forecasts,” “targets,” or future or conditional verbs, such as “will,” “should,” “could” or “may,” and variations of such words or similar expressions are intended to identify forward-looking statements. These forward-looking statements, including, without limitation, management’s examination of historical operating trends and data, are based upon our current expectations and various assumptions and beliefs. In particular, such forward-looking statements are subject to uncertainty and changes in circumstances and involve risks and uncertainties that may affect the Company’s operations, markets, products, prices and other factors as discussed in the Company’s filings with the Securities and Exchange Commission (the “SEC”). In addition, there can be no assurance that the review of the Textile Effects Division will result in one or more transactions or other strategic change or outcome. Significant risks and uncertainties may relate to, but are not limited to, ongoing impact of COVID-19 on our operations and financial results, volatile global economic conditions, cyclical and volatile product markets, disruptions in production at manufacturing facilities, timing of proposed transactions, reorganization or restructuring of the Company’s operations, including any delay of, or other negative developments affecting the ability to implement cost reductions and manufacturing optimization improvements in the Company’s businesses and to realize anticipated cost savings, and other financial, operational, economic, competitive, environmental, political, legal, regulatory and technological factors. Any forward-looking statement should be considered in light of the risks set forth under the caption “Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2021, which may be supplemented by other risks and uncertainties disclosed in any subsequent reports filed or furnished by the Company from time to time. All forward-looking statements apply only as of the date made. Except as required by law, the Company undertakes no obligation to update or revise forward-looking statements to reflect events or circumstances that arise after the date made or to reflect the occurrence of unanticipated events. Non-GAAP Financial Measures: This communication contains financial measures that are not in accordance with generally accepted accounting principles in the U.S. (“GAAP”), including adjusted EBITDA and free cash flow. For more information on the non-GAAP financial measures used by the Company and referenced in this communication, including definitions and reconciliations of non- GAAP measures to GAAP, please refer to the “Non-GAAP Reconciliation” hyperlink available in the “Financials” section of the Company’s website at www.huntsman.com/investors. The Company does not provide reconciliations of forward-looking non-GAAP financial measures to the most comparable GAAP financial measures on a forward-looking basis because the Company is unable to provide a meaningful or accurate calculation or estimation of reconciling items and the information is not available without unreasonable effort. This is due to the inherent difficulty of forecasting the timing and amount of certain items, such as, but not limited to, (a) business acquisition and integration expenses, (b) merger costs, and (c) certain legal and other settlements and related costs. Each of such adjustments has not yet occurred, are out of the Company’s control and/or cannot be reasonably predicted. For the same reasons, the Company is unable to address the probable significance of the unavailable information. Please vote your shares by telephone or by Internet TODAY, by following the simple instructions on the WHITE proxy card. If you have any questions about how to vote your shares, please call the firm assisting us with the solicitation of proxies: Innisfree M&A Incorporated Shareholders may call toll-free: 1 (877) 750-0926 Remember, please do not vote using any blue card you may receive from Starboard. Use only the WHITE proxy card to vote TODAY for all of Huntsman’s highly qualified director nominees. |